Having a good working knowledge of the different methods available for calculating the present value of future lost income in personal injury and wrongful death cases gives an expert an opportunity to demonstrate his or her expertise in the forensic economic field. This article will visit three methods and expand on their similarities and differences.

The U.S. Supreme Court, various Federal Circuit Courts of Appeal, and numerous state Supreme Courts have provided decisions highlighting three different methods available for calculating the present value of future lost income in personal injury and wrongful death cases. These methods are discounting using the real interest rate, discounting by market interest rates, and total offset. Having a good working knowledge of these three methods gives an expert an opportunity to properly calculate the present value of future losses and demonstrate his or her expertise in the forensic economic field.

Discounting Losses to Present Value in Personal Injury Cases

Last June, I published an article in QuickRead arguing it was essential for financial or economic experts working in the personal damages area (personal injury or wrongful death) to review the U.S. Supreme Court’s decision in the Pfeifer v. Jones Laughlin Steel Corp. case.[1] [2] In that article, I discussed the three methods offered by the court for discounting future losses or costs to present value in personal damages cases. This article will revisit those three methods and expand on their similarities and differences.

The Pfeifer decision discussed the three methods available for discounting future losses to present value: discounting by the real interest rate, discounting by market interest rates, and total offset.[3] The 5th Circuit Court of Appeals provided greater detail into these three approaches in its Culver v Slater Boat Co. decision.[4]

In the Culver decision, the 5th Circuit defined the case-by-case, below market discount, and total offset methods in this way.

“As the Court noted in Pfeifer, three methods are available for adjusting damage awards to account for the effect of inflation. In the case-by-case method, the factfinder is asked to predict all of the wage increases a plaintiff would have received during each year that he could have been expected to work, but for his injury, including those attributable to price inflation. The prediction allows the factfinder to compute the income stream the plaintiff has lost because of his disability. The factfinder then discounts that income stream to present value, using the estimated after-tax market interest rate, and the resulting figure is awarded to the plaintiff.

In the below market discount method, the factfinder does not attempt to predict the wage increase the plaintiff would have received because of price inflation. Instead, the trier of fact estimates the wage increases the plaintiff would have received each year because of all factors other than inflation. The resulting income stream is discounted by a below market discount rate. This discount rate represents the estimated market interest rate, adjusted for the effect of any income tax, and then offset by the estimated rate of general future price inflation.

The third method is the total offset method. In this calculation, future wage increases, including the effects of future price inflation, are legally presumed to offset exactly the interest a plaintiff would earn by investing the lump-sum damage award. Therefore, the factfinder using this method awards the plaintiff the amount it estimates he would have earned, and neither discounts the award or adjusts for inflation.”[5]

Applying the Three Methodologies

The method most commonly used for discounting future losses or costs to present value will vary from state to state. However, any method used will be a derivation of the three mentioned in the Pfeifer and Culver decisions. All of these methods are based on how to evaluate inflation in growing and discounting future monies to present value.

Total Offset Method

“Beaulieu v Elliott, 434 P.2d 665 (Alaska, 1967) set the pattern many years ago for calculating losses using a very simplified method. The basic assumption is that the rate of growth in wages will be exactly to, and thus offset, the rate of interest available on safe investments. To determine the loss, then, one need only know the amount of earnings at the time of the incident and the number of years remaining that the plaintiff would have worked, viz loss duration. Because of the total offset, there is no need to project future wage increases, nor is there a need to convert future wages to present value. Simply multiply the wages at the time of the incident by the number of years to be worked and the result is the loss.”[6]

For many years, Pennsylvania was the only state expecting personal injury losses to be discounted to present value by the total offset method. Lawrence Grant’s article on discounting methods in Pennsylvania provides the following information regarding the states move to total offset. “The Pennsylvania Supreme Court recently [1980] ended a swirl of ever-changing rules and evidentiary requirements concerning damages for future loss of earnings in Kaczkowski v Bolubasz.[7] Pennsylvania has now adopted what may be labeled a ‘total offset’ approach to inflationary aspect of such future damages and permits evidence of increased productivity regarding the victim’s future year’s earnings to present value by the ‘real’ discount rate.

The Kaczkowski court adopted the ‘total offset method’. The court recognized the method’s convenience and relied on the premise that ‘future inflation rates and future interest rates do not exist in a vacuum but co-vary significantly.’ The court also observed that the ‘total offset method’ obviously achieves the goals of efficiency and predictability in damage award computations, and more satisfactorily achieves the goal of accuracy than would a method which uses an inflation factor derived from a periodic reevaluation of the volatile inflation rate.”[8]

Recently, Pennsylvania began to adopt the case-by-case or below market discount rate methods for estimating the present value in medical malpractice litigation. But, the remainder of personal damages cases must use total offset for calculating the present value of future losses.

Case-by-Case Method

This method calls for the expert to determine an appropriate growth rate including real and inflationary factors, if appropriate, and grow the plaintiff’s annual income yearly by the determined annual growth rate. Each future year’s income is then discounted to present value by the appropriate, current, risk-free rate.

“When words like standard or traditional are applied to a technique, they do not necessarily mean that the method is best and most accurate. Instead, they usually denote the fact that it was the first method used in a particular situation. Such is the case with the nominal rates method which has been in literature for many years. A nominal value is a value that actually exists and has not been modified by removing inflation or anything else. For example, if the interest yield on a 10-year U.S. Government Bond is 2.3% in 2019, then that is the actual, or nominal rate. Likewise, if journeyman ironworker wages increased 3.0% from 2018 to 2019, then 3.0% is the nominal increase with no alterations made to it.”[9]

Below Market Discount Rate Method

When using the below market discount rate method, the expert “does not attempt to predict the wage increase the plaintiff would have received as a result of price inflation. But instead, ‘estimates the wage increase the plaintiff would have received each year as a result of all factors other than inflation.’”[10]

By allowing for the use of the below market discount rate method, the courts are saying experts can, and in some cases should, use a real rate of return method. “In economics, the term ‘real’ refers to some value from which inflation has been removed. An approach to evaluations used by some economists is to remove inflation from wage increases and to also remove inflation from interest rates. The result is real wage changes and a real rate of interest. The difference between using real rates and total offset is quite subtle. In the offset method, the economist is assuming that the wage growth rate and the interest rate are equal and ‘offset’ each other. The real rates method more closely resembles the nominal rates method with the difference being only that inflation has been removed. … Assume the nominal growth rate in wages is 4% and that inflation is 2%. Subtraction tells us that the real growth rate is the difference between the two or 2%. Then assume the nominal interest rate is 6%. After removing inflation, the real interest rate becomes 4%. The economist’s calculation is then made by increasing wages at a 2% real rate for future years and then discounting those wages by 4% real interest. There is nothing wrong with this method, but the economist [financial expert] should be able to provide … the three elements that are needed to work in real rates: the nominal wages growth rate, the nominal interest rate, and the rate of inflation. Without knowing these, (s)he will have difficulty justifying the real rates (s)he is using. The reality is that, if done correctly, using real rates results in the same value of the loss as will be found by using nominal rates.”[11]

Showing Work for Each Method

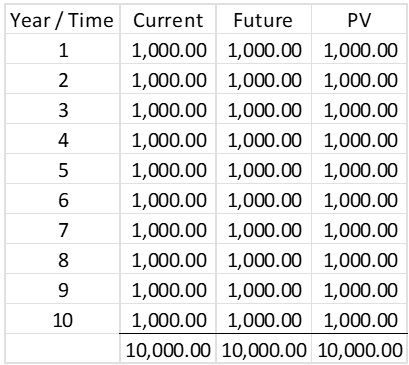

To show how these three methods work, assume there is a loss of income of $1,000 per year for 10 years in the future. Research has shown that the projected inflation rate over that period will be a nominal 2.50%. The risk-free interest rate for that same time will be a nominal 3.0%.

For total offset, the assumption would be that the interest rate and the growth (inflation) rate would be the same. Therefore, the annual loss is not grown nor discounted. The results appear this way:

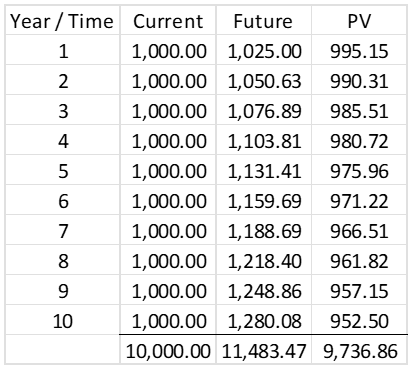

The case-by-case method uses nominal rates. For this analysis, the lost income is grown each year by 2.5%, the nominal growth rate, and the future income values are then discounted by 3.0%, the nominal interest rate. The results appear this way:

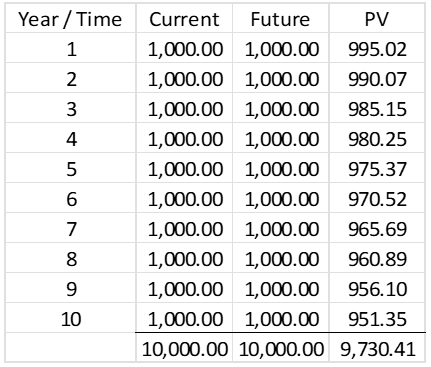

The below market discount rate provides a real rate of return estimate. For this calculation, the inflation rate, 2.50%, is subtracted from the nominal growth rate and the nominal interest rate. If these calculations assume the growth rate and the inflation rate are the same, then 2.50% minus 2.50% equals 0.0%. Therefore, the future income does not grow annually. When 2.50% is subtracted from 3.0%, the difference is 0.50%. This percentage becomes the real interest rate. This real interest rate becomes the discount rate or the below market discount rate. The results appear this way:

There is a $6.45 difference between the nominal results and the real rate results. Most of this is attributed to the mathematical way of calculating the real rate. What has been shown so far is the arithmetic way to calculate the below market discount rate. There is a geometric way of making such a calculation.

The concept for the below market discount rate is based on the Fisher equation.[12] The Fisher equation is a concept in economics that describes the relationship between nominal and real interest rates under the effect of inflation. The equation states that the nominal interest rate is equal to the sum of the real interest rate plus inflation. If you subtract the inflation rate from the nominal interest rate, you will know the real interest rate. The same concept applies to the nominal growth rate.

While experts subtract inflation from the nominal rates, some economists believe a geometric not arithmetic technique should be used. Rather than the straightforward 3.0% nominal interest rate minus 2.50% inflation rate for a real interest rate of 0.50%, the geometric model appears this way:

Where:

i equals the nominal interest rate,

g equals the nominal growth rate.

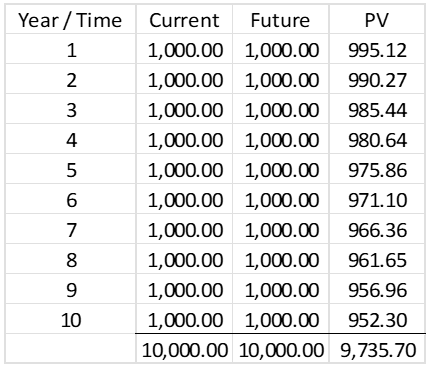

The result is the real interest rate or, for these purposes, the real discount rate. The result of this calculation is 0.49%.

When this real interest rate is used to discount the future income stream, the results appear this way:

This result is only $1.16 different from the case-by-case, nominal results, confirming the nominal and real calculations provide very similar results. The arithmetic subtraction provided a difference of 0.07% from the case-by-case result. While the geometric calculation provided a difference of 0.01%.

With this being only a slight difference, many experts prefer to use the arithmetic method because it is easier to explain to the trier-of-fact.

Interest Rates, Growth Rates, and Taxes

One issue not discussed in this article is the choice of nominal interest rates to be used for discounting. These can include current rates from a singular yield on a risk-free security maturing in 20 years for a 20-year loss period or a laddered portfolio of risk-free bonds that include both short-term and long-term bonds that mature during the loss period. It could include historical or forecast interest rates. Using these various sources for the nominal interest rate have pros and cons. The same is true with the issue of selecting appropriate nominal growth rates. They may be based on historical, current, or projected future rates. These nominal growth rates will include inflation as well as merit, productivity, or bonus pay which usually make anticipated future annual pay increases greater than inflation.

Then there is consideration for income taxes. Many states do not require adjusting the income stream for income taxes. Other states and the federal courts generally do require such an adjustment. The handling of taxes and how the inclusion of income taxes impacts the interest rates used in discounting future losses to present value is a third issue deserving review.

These topics deserve to be covered in greater discussion at another time.

Conclusion

Because the standards may vary from state to state, an expert should discuss with the hiring attorney the court standards in the jurisdiction of the assignment. As a couple of quick examples, most states prefer nominal or real rate calculations, but Pennsylvania wants the total offset method used except in medical malpractice suits. Michigan will accept nominal growth rates but a statutory discount rate must be used. Knowing all the options for discounting future losses to present value is one thing but it must be combined with knowing what courts expect to see in the jurisdiction of the assignment.

[1] Calculating Personal Damages: A Review of the U.S. Supreme Court’s Pfeifer Decision, Allyn Needham, QuickRead, 6/11/2025, https://quickreadbuzz.com/2025/06/11/litigation-allyn-needham-calculating-personal-damages/

[2] Jones Laughlin Steel Corp. v Pfeifer, 462 U.S. 523, (1983).

[3] Jone Laughlin Steel Corp. v Pfeifer, 462 U.S. 523, 542-544, (1983).

[4] Culver v Slater Boat Co., 722 F.2d 114, (1983). This is referred to as the Culver II decision. This decision came from a rehearing by the 5th Circuit. Earlier, they had reversed and remanded part of the lower court’s decision.

[5] Culver v Slater Boat Co., 722 F.2d 114, 118, (1983).

[6] Determining Economic Damages, Revision 29, Gauri Prakash-Canjels, PhD, James Publishing Co., 2025, p.1202.

[7] Kaczkowski v Bolubasz, 491 Pa. 561, (1980).

[8] Damages for Loss of Future Earnings in Personal Injury Awards – Pennsylvania Locks Its “Revolving Dorr Approach, Lawrence Evans Grant, Penn State University, Dickinson Law Review, Issue 1, Vol. 87, 1982–1983, https://insight.dickinsonlaw.psu.edu/dira/vol87/iss1/2

[9] Ibid, 1203.

[10] Culver v Slater Boat Co., 722 F.2d 114, 118, (1983).

[11] Determining Economic Damages, Revision 29, Gauri Prakash-Canjels, PhD, James Publishing Co., 2025, p.1203.

[12] Irving Fisher, American Economist and Statistician, is most famous for developing the Quantity Theory which is shown as MV=PQ. He also provided an equation for examining the relationship between inflation and real rates of return. This second equation has been used as a basis for the below market discount rate.

Allyn Needham, PhD, CEA, is a partner at Shipp Needham Economic Analysis, LLC, a Fort Worth-based litigation support consulting expert services and economic research firm. Prior to joining Shipp Needham Economic Analysis, he was in the banking, finance, and insurance industries for over 20 years. As an expert, he has testified on various matters relating to commercial damages, personal damages, business bankruptcy, and business valuation. Dr. Needham has published articles in the areas of financial and forensic economics, and provided continuing education presentations at professional economic, vocational rehabilitation, and bar association meetings. In 2021, Dr. Needham received a NACVA Outstanding Member Award. He is also a member of NACVA’s QuickRead Editorial Board.

Dr. Needham can be contacted at (817) 348-0213 or by e-mail to aneedham@shippneedham.com.