WikiLeaks Delivers—Valuation Reports From Top Firms (Deloitte, KPMG, E&Y, Houlihan & SVB)

Benchmarking Your Reports and Examining What Hypothetical Conditions and/or Extraordinary Assumptions You Have Made!

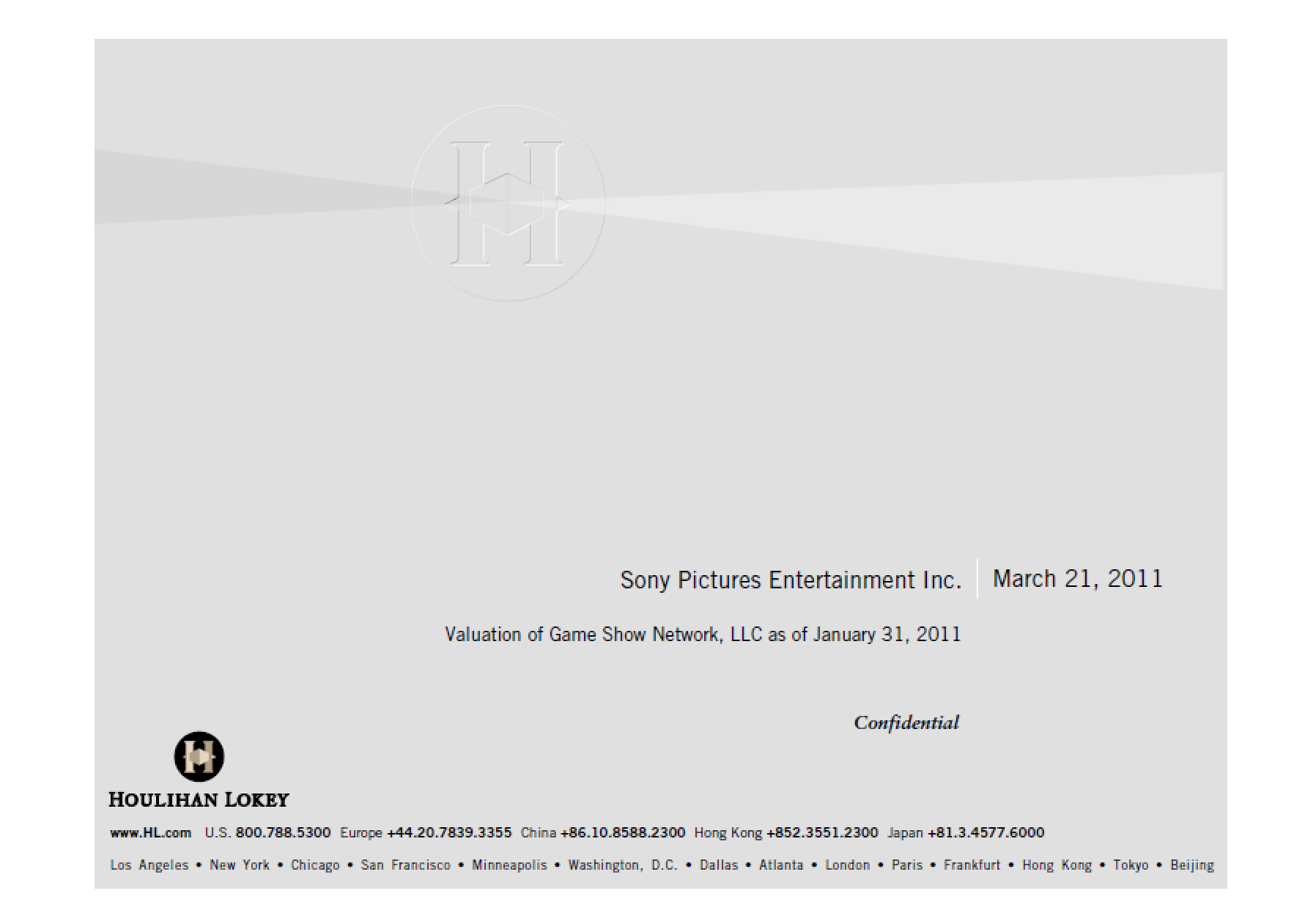

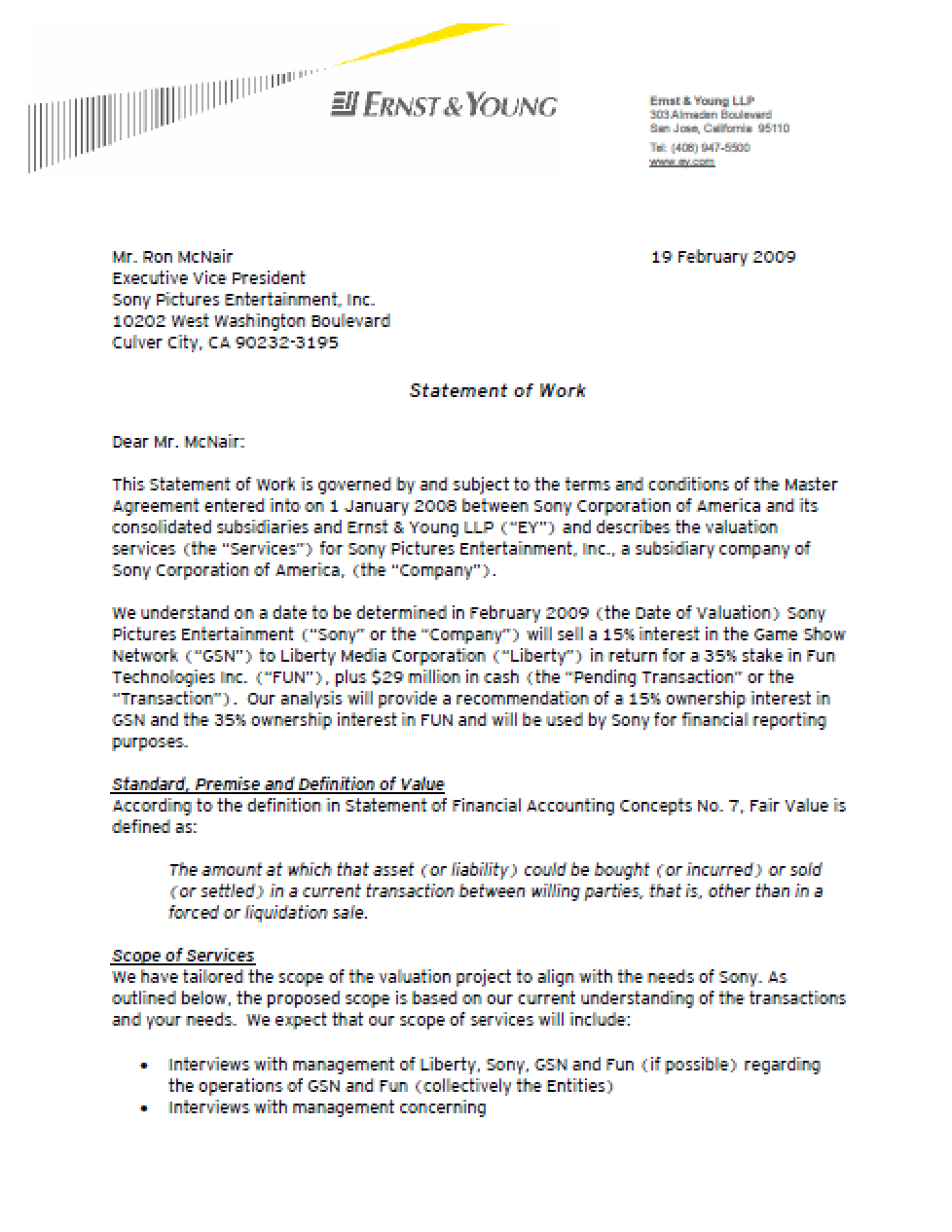

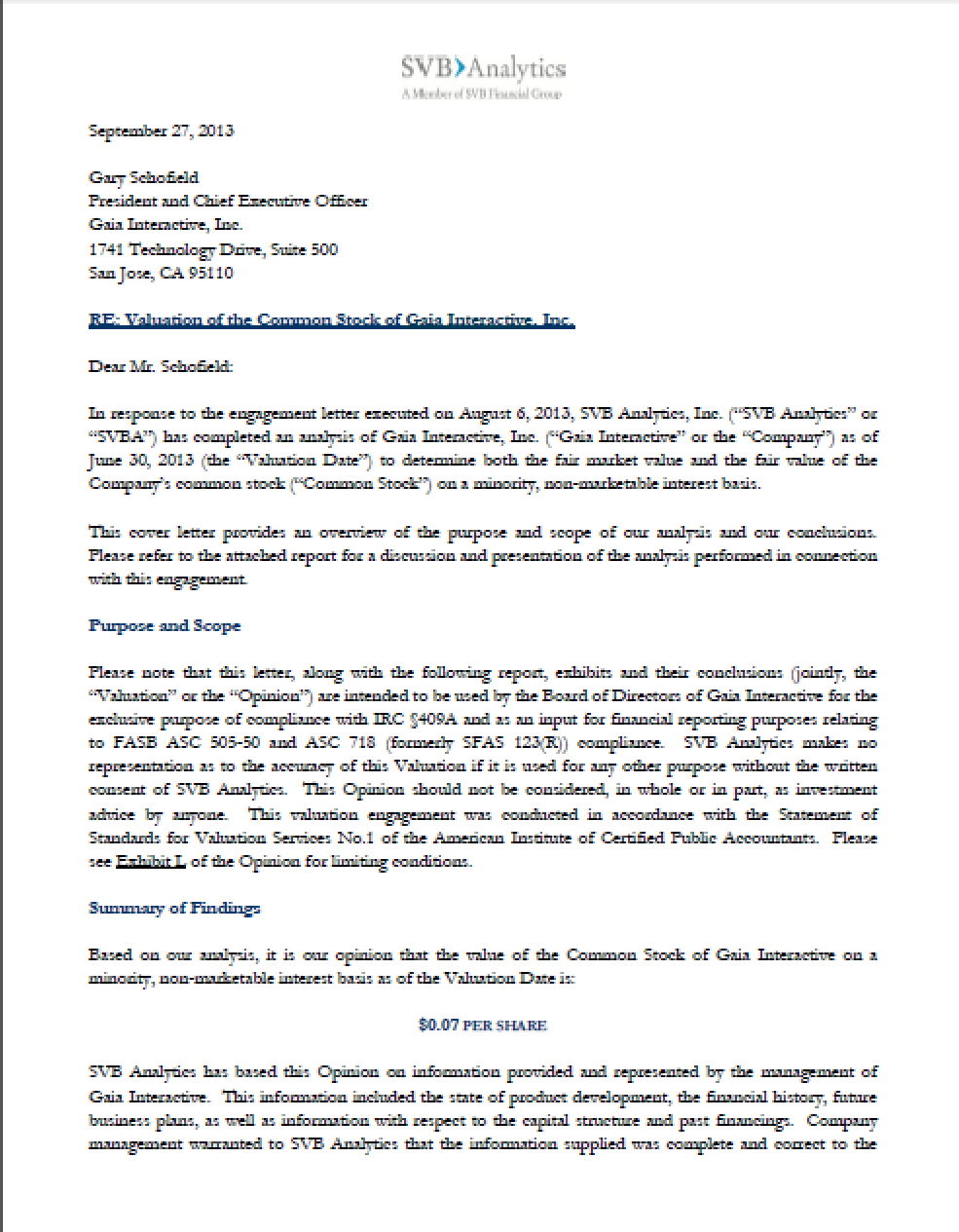

However, thanks to WikiLeaks, “The Interview”, and Sony Pictures, a rather sizeable repository of sample reports exist free of charge. These reports, as you might expect, are from the transaction arms of Big Four firms as well as leading national shops. Anyone who has been doing this for a while has seen valuation reports from almost every large firm out there. But for those new to the profession, or people helping others along, these now public documents are of educational value, in my opinion.

I am often asked for sample valuation reports from students just getting their valuation credential. Naturally, our valuation reports cannot be shared with students since they are confidential client property. In most cases, I simply refer them to NACVA’s report library; in other cases, I forward sample cover sheets used in our conclusion of value reports with the caveat that our report covers are not typical of what we see from most firms.

I am often asked for sample valuation reports from students just getting their valuation credential. Naturally, our valuation reports cannot be shared with students since they are confidential client property. In most cases, I simply refer them to NACVA’s report library; in other cases, I forward sample cover sheets used in our conclusion of value reports with the caveat that our report covers are not typical of what we see from most firms.

However, thanks to WikiLeaks, “The Interview”, and Sony Pictures, a rather sizeable repository of sample reports exist free of charge. These reports, as you might expect, are from the transaction arms of Big Four firms as well as leading national shops. Anyone who has been doing this for a while has seen valuation reports from almost every large firm out there. But for those new to the profession, or people helping others along, these now public documents are of educational value, in my opinion.

An example of how I referenced links to the reports to explain an important USPAP related concept to a new valuation professional follows below.

USPAP Hypothetical Conditions and Extraordinary Assumptions

One of the most common recommendations I make to NACVA members who don’t hold an ASA credential is to remove the phrase, “in accordance with…the Uniform Standards of Professional Appraisal Practice (“USPAP”)” from their reports unless two very important conditions were met before placing that phrase in their work product:

- The business valuator has actually taken a USPAP course and exam (or at the very least spent 20 hours or so getting familiar with USPAP on their own), and

- The business valuator is 100% sure that their report has in fact been developed in accordance with USPAP.

I’ve had very experienced professionals, including CVAs, ASAs, CBAs, and CFAs tell me they were 100% certain their reports were in fact in accordance with USPAP. As a quick test, I ask two questions:

- Are any hypothetical conditions or extraordinary assumptions used in your analysis?

- If yes, were they identified and defined in accordance with USPAP?

In eighty percent of the cases I get an inconsistent response as to what a hypothetical condition is and that is totally understandable. However, if a valuator is unclear on what a hypothetical condition is and defining a condition, if present, is required by USPAP, then obviously the valuator’s assertion of “…in accordance with USPAP” is immediately put into question, I believe.

Some of the USPAP language describing what a hypothetical condition and what an extraordinary assumption is, is less than user friendly. Here are a couple of tests I have recommended in the past to help people overcome some of the wordiness in the definitions. If you disagree, please let me know (just send me a LinkedIn Message to the account below).

Simple Test:

Are you sure it was untrue as of the valuation date?

IF YES, It is not an extraordinary assumption as defined by USPAP.

It may be a hypothetical condition.

Are you unsure if it was true as of the valuation date?

IF YES, It is not a hypothetical condition as defined by USPAP.

It may be an extraordinary assumption.

Now for the definitions from USPAP, as presented on Wikipedia:

“Extraordinary assumptions are defined as assumptions, directly related to a specific assignment, which, if found to be false, could alter the appraiser’s opinions or conclusions. A comment to the definition explain that extraordinary assumptions presume as fact otherwise uncertain information about physical, legal, or economic characteristics of the property,

- or about conditions external to the property, such as market conditions or trends,

- or about the integrity of data used in an analysis.

Hypothetical conditions are defined as that which is contrary to what exists but is supposed for the purpose of analysis. The comment to the definition explain that hypothetical conditions assume conditions contrary to known facts about physical, legal, or economic conditions,

- or about conditions or facts lying outside the observable scope of discussion or analysis but potentially affecting the scope or results of analysis or direction of discussion (such as market conditions or trends known to be contrary to known conditions),

- or about the accuracy, reliability, or integrity of data on which an analysis may be based.”

ASA’s Business Valuation Standards offer a more concise definition:

“Hypothetical Condition. That which is contrary to what exists but is supposed for the purpose of analysis.”

In my experience with accountants and others, the AICPA definition of a “hypothetical assumption” which is a bit more intuitive in the context of projections, is often confused with the USPAP and AICPA definitions of a hypothetical condition [emphasis added].

AICPA—AT Section 301, Financial Forecasts and Projections:

“Hypothetical assumption—An assumption used in a financial projection to present a condition or course of action that is not necessarily expected to occur, but is consistent with the purpose of the projection.”

“Hypothetical conditions affecting the subject interest may be required in some circumstances. When a valuation analyst uses hypothetical conditions during a valuation or calculation engagement, he or she should indicate the purpose for including the hypothetical conditions and disclose these conditions in the valuation or calculation report…”

Free Challenge

Using any of the published valuation reports on WikiLeaks, or if you are willing to look at your own reports, ask yourself:

- Are any hypothetical conditions or extraordinary assumptions made or used in your analysis?

- If yes, were they properly identified and defined in accordance with USPAP?

Please let me know what you discover. Further, if you agree or disagree with the premise that they should be defined and disclosed as such, or if you feel that I am totally off base in using this as a quick test to determine if certain reports are in fact in accordance with USPAP, please send me a direct message on Twitter or LinkedIn. We’ll publish the comments you send in the next post on this topic.

For the record, most of the reports I encounter in the regular course of business could not be completed without at least one hypothetical condition and, in many cases, an extraordinary assumption. I recognize this is not the case for many practice areas.

I look forward to your input.

Lorenzo Carver, MS, MBA, CVA, ABV, CPA is Founder and CEO of Liquid Scenarios, an automated valuation software, data, and services company responsible for the first one click valuation solution for complex, illiquid securities. He is the inventor of the Carver Import Algorithm, Search2Model, a patented valuation technology and author of Venture Capital Valuation published by John Wiley & Sons. Mr. Carver has over 40,000 hours of valuation related experience and his Liquid Scenarios automated valuation software, services and data is used to value thousands of venture backed companies, including industry changing successes like Facebook, Twitter, Dropbox and Uber.

Mr. Carver can be reached at: (650) 690-2169 or e-mail to: bpcentral@gmail.com.

Related posts

-

Unimpeachable Substance and Principles

-

AI, Ethics, and Standards in Valuation Practice

-

The Unit Valuation Principle for Property Tax Purposes

-

The Unit of Valuation Principle for Property Tax Purposes

-

Marketing Isn’t About Us

-

Measuring Damages Involving Individuals

-

Should AI be Disclosed?

-

")

A Valuation Primer for Renewables (Part II)