Does the IRS or Anyone Care? (Part II of II)

Part one of this article presented the “current method” and “option pricing method” (OPM) for allocating value to common stock for 409a valuations, and how these two methods differ in pricing of common stock. Part two examines the implied changes made by OPM and how it affects stakeholders. The article begins with a brief review of the key impacts on the valuation problem.

[su_pullquote align=”right”]Resources:

[su_pullquote align=”right”]Resources:

Business Valuation Venture Capital Forum

History and Evolution of the FMV Opinion Market -Sizing the FMV Market

Review of Option-based Models for Discount for Lack of Marketability

Valuing Complex Financial Instruments—Monte Carlo Simulation and Lattice Models

[/su_pullquote]

Part one of this article presented the “current method” and “option pricing method” (OPM) for allocating value to common stock for 409a valuations, and how these two methods differ in pricing of common stock. Part two examines the implied changes made by OPM and how it affects stakeholders. We start with a brief review of the key impacts on the valuation problem.

OPM Impacts on the Valuation Problem

As discussed in part one, OPM implicitly changes the valuation problem. The conflicts between OPM and current value allocation are:

Change in Valuation Subject: OPM shifts the subject of valuation to partial equity interests, versus the company.

Shift in Valuation Date: Applying probabilities based upon a future exit event moves the valuation date to an arbitrary future date from the present.

Market: Another alteration is replacement of the hypothetical fair market value (FMV) prudent buyer with a faceless market.

Common Sense: The pattern of purchase by angel investors and venture capital companies points to a reduction in value for common stock, and a premium for the preferred interests. OPM often has the opposite effect.

Accounting Practice: Attempting to compare future values with present values violates accrual accounting principles because future value cannot be earned at the date of valuation.

Once we shift from the control interest to a partial interest, we must also deal with other features of equity blocks. So another important consideration is the type II error—what is missing from OPM.

Minority Interests and FMV

We see that OPM makes relative shifts in the allocation of equity between blocks. Valuing equity blocks increases valuation complexity in a quantum jump because we enter the arena of Discounts for Lack of Marketability (DLOM) to meet the FMV standard of value. To determine relative values between classes, a post OPM DLOM analysis would compare the remaining features and cash flows associated with each equity block to one another. It is a Pandora’s Box we do not want to open.

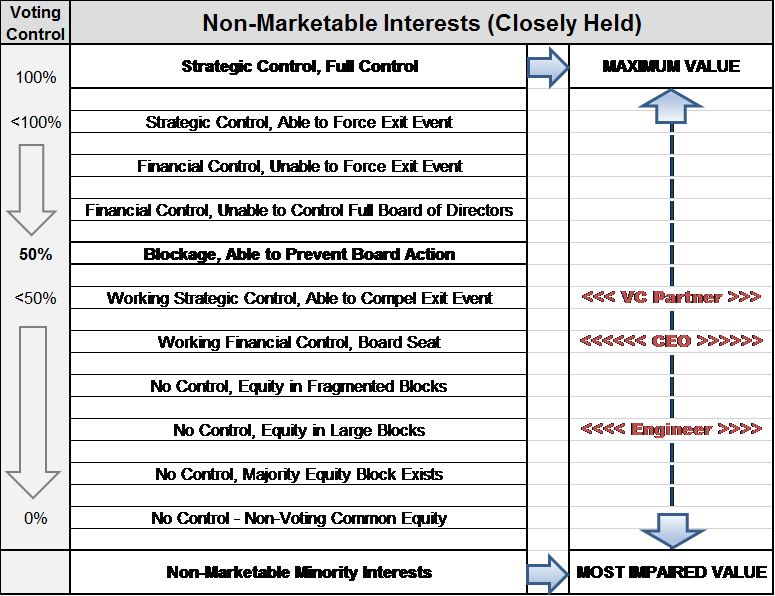

On top of equity characteristics, once the seal has been broken on judging value between classes, the entire cap table of individual stockholders is drawn into the analysis. DLOM compels us to analyze control influence by the grantee on each issuance. For example, stock option grants to the CEO would have a different strike price than those granted to an engineer, because the CEO has operational control of the company.

For those unfamiliar with the factors involved in establishing a DLOM, the following two charts are presented. The first chart identifies control levels typically used in a DLOM analysis and where the interests would fall for degree of control.

Chart I: Value Impairment for Control

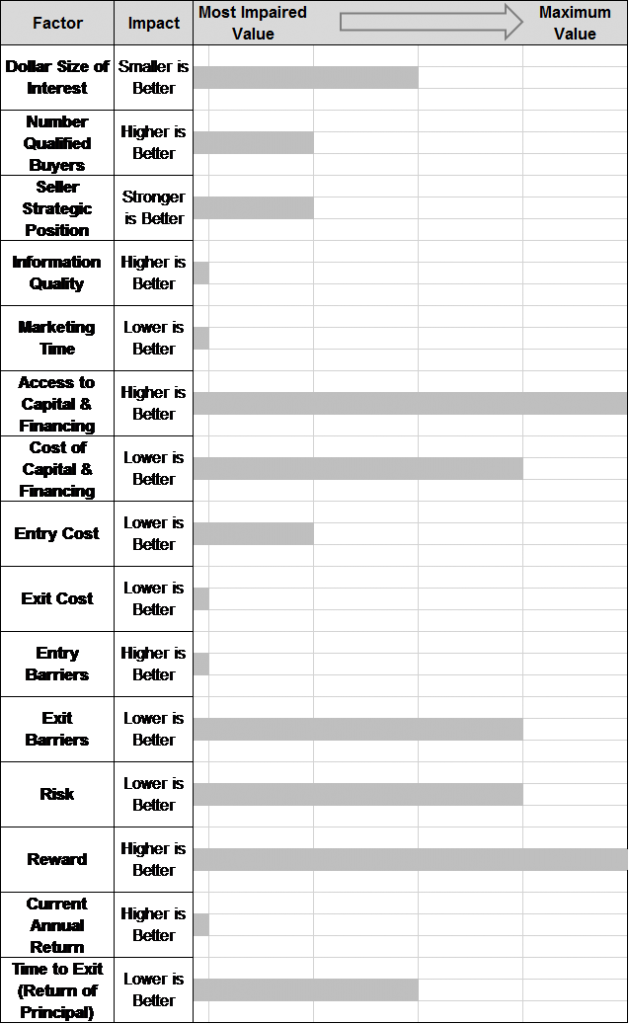

And then we would also need to deal with other features of different equity securities and compare them on marketability factors. These factors look like this:

Chart II: Value Impairment for Security Features

A comprehensive analysis of partial interests would require applying all factors relevant to the problem, not only the potential for a distribution from an exit event. Only with a strap-on DLOM comparative analysis can an OPM be justifiably incorporated into the valuation. Otherwise, it is a biased, one-dimensional misapplication of technique.

Regulatory Issues

Based on the above arguments, OPM meets neither the fair value (undiscounted) or FMV (discounted) standard of value called out in tax related government regulations, and many company agreements. The analysis is incomplete, so it becomes its own unique value standard.

Being non-compliant with FMV is a vulnerability. It opens the door to all kinds of challenges. The non-compliance issue may be used by an attorney to have a company’s historical valuations thrown out as evidence in a dispute. The company would then have no basis to present its value to the court, and the opposing expert’s reports would control the question.

Court opinion is already established around formula approaches, as the Tax Court does not find them to be reliable. IRS Revenue Ruling 68-609 states that the formula method “should not be used if there is better evidence available from which the value of intangibles can be determined.” In this regard, the trustworthiness of OPM output is low. The M-B-S formula is highly sensitive to volatility and time to exit, so small changes in these inputs create a wide variation of results. OPM is not only a weak scheme, highly sensitive formulas in general do not produce accurate outcomes. Considering that true volatility of the company’s equity is zero, and the time to exit is likely to be a hopeful guesstimate, identifying values to enter into the formula is problematic. If used, some kind of responsiveness test should be added. Sensitivity analysis is demanded for ESOP valuations. Why not 409a valuations?

On the legal front, treasury regulations appear to preclude substituting a public market security as a proxy for the subject being valued. Per IRS Revenue Bulletin 2007-19, section 3b, “The Treasury Department and the IRS believe that the stock right exception under section 409a was intended to cover stock rights directly reflecting the enterprise value of the entity for which the service provider is providing services” (italics added). OPM appears to be an indirect methodology using proxies for the actual subject.

And our professional standards get in the way. NACVA requires its practitioners to obtain sufficient relevant data on which to base their conclusion. Using only one factor, market volatility, to adjust equity block values, is an incomplete analysis. Evidence exists that other factors, such as control and marketability features, need to be considered. This professional standard is especially worrisome for those valuations using only a previous financing as their sole starting point for determining current value.

Effects of OPM

- It is a popular method. So, what is the effect of shifting to valuing shares based on future exit value probabilities? Answer: A false sense of security. Mispricing. Poor alignment of performance goals with actual value. Deceiving the workforce.

Setting the strike price of an option at a premium is not an IRS problem. The compliance risk only comes when common stock suffers a reduction in value. That becomes a cause for concern if common stock value falls below FMV and triggers a taxable event.

Practically, however, OPM has significant room in which to err under 409a compliance, because IRS regulations just ask us to define if a taxable income event has occurred. If the strike price of the option grant is above the regulatory minimum at the time the board approves it, no income tax is incurred.

Setting Strike Price

The minimum value for the strike price is FMV, which includes a discount for Lack of Marketability (DLOM) for non-marketable, non-control interests. However, since we typically want to avoid dilution of existing shareholders, we normally issue new options at Fair Value—the undiscounted value. This practice is documented in accounting directive ASC 718. Fair value allows us a 20%–50% margin for error.

Setting option strike prices at fair value is the best practice. It is equitable to the company, existing shareholders, and grantee. It not only deters shareholder suits over unfair dilution, it ensures that the option program provides market rate capital infusions to the company over the long run. Because when the options are redeemed, the option premium is paid to the company, adding to its cash position.

Who Cares if we Use OPM?

The IRS is looking for untaxed income, so it is doubtful they will challenge OPM when its use is not expected to reduce value of common stock below FMV. Using OPM for option strike prices has risks, but if the starting current value is soundly developed, the typical unused 20%–50% DLOM would keep most cases above FMV.

As the weakest link in the chain, though, OPM can be attacked for FMV compliance to get an entire valuation thrown out. All that needs to be established is that the value conclusion does not meet FMV standards. Then the company is left with no evidence to support its valuation in court.

Executives and other employees may take an interest in the unique “OPM standard of value” if they feel that the strike price is being unfairly inflated or depressed. The effect is important at the time a grantee receives their options, but also when other grantees get awards afterward. When exits go bad, this is one area where litigation ensues over valuation.

The ones most at risk are CEOs, who are generally the largest benefactors of option grants. If the share price is set in error, they are either accused of unjustly enriching themselves at the expense of other shareholders, or they are cheated out of gains they have rightly earned.

But the true tragedy of OPM happens when non-executive employees commit their careers to a venture, exchanging salary for equity. With companies remaining private longer today, these commitments may now span a decade of service. As their stock grants are given increasing strike prices, purported to be FMV, the key employees believe that they are building wealth. They may even buy stock at these values. Then, the long-awaited exit comes, and these employees find their stock options out of the money because the common stock price is inflated no longer. When the exit occurs, equity blocks can no longer be manipulated by applying mythical volatility, and the current value is at hand. Executives and directors should know better, but engineers, scientists, and sales professionals investing their best moneymaking years in the company are victims of a charade.

Back to Current Value

If we avoid OPM, we never open Pandora’s Box of having to value equity based on the grantee, nor do we place the CEO and board of directors in jeopardy. Fairness is more assured and the valuation baseline is consistent with any exit. All the complexities of valuing partial interests resolve if we simply use the current value of company equity, and traditional waterfall analysis. Importantly, the precepts of accrual accounting and FMV are satisfied as we match all earned value and efforts into the same time period.

OPM is a solution looking for a problem to solve. It does not reflect reality, and is not worth the risk, the additional cost, or the ruin of workforce spirit that occurs when its defects are revealed.

[divide]

James A. Lisi is a partner and valuation expert at American ValueMetrics Corporation with over twenty-five years in executive and strategic positions in Fortune 100, Private Equity and his own personally held businesses. His opinions of value are analytically sound, market based, and highly defensible—presented in formats and methodologies that are highly respected by the Tax Court and investors alike. He has been valuing businesses with American ValueMetrics for more than twelve years and is a member of the National Association of Certified Valuators and Analysts (NACVA), holding the Certified Valuation Analyst (CVA) designation. He is a California state-appointed member of the California Coastal Loan Committee, a member of Premier Professionals of Santa Barbara, Santa Barbara Professional Advisors, Rotary International, and the California Coast Venture Forum.

Mr. Lisi can be reached at (805) 797-1710 or by e-mail to jim@sbvaluations.com or james.lisi@americanvaluemetrics.com.