A Legislative Approach?

In April of 2023, the United States Department of Labor (DOL) committed to move forward with a regulation to clearly detail “adequate consideration” in section 408(e) of the Employee Retirement Income Security Act of 1974 (ERISA). For decades the DOL has utilized litigation versus heeding Congress’s edict to enact regulations regarding adequate consideration and it seems as though action is going to finally be taken. This article discusses recent developments suggesting a change in their approach.

In April of 2023, the United States Department of Labor (DOL) committed to move forward with a regulation to clearly detail “adequate consideration” in section 408(e) of the Employee Retirement Income Security Act of 1974 (ERISA). This most recent DOL Employee Stock Option Plan (ESOP) legislative initiative was brought about in September of 2022[1] by The ESOP Association (TEA) via a “Petition for Notice-and-Comment Rulemaking Regarding the Definition of Adequate Consideration Under Section 408(e) of the ERISA”.[2] The TEA is just one of many who have been seeking formal rules to be put in place to ensure that those involved in ESOP transactions (trustees, sellers, participants) are participating in transactions at fair market value and that the ESOP is not overpaying for companies that are being bought on the employee owners’ behalf. For decades the DOL has utilized litigation versus heeding Congress’s edict to enact regulations regarding adequate consideration and it seems as though action is going to finally be taken. This article discusses recent developments suggesting a change in their approach.

Background—ESOPs

ESOPs are employee benefit plans, or tax-exempt trusts, funded by tax-deductible contributions from the company. ESOPs enable ownership of part or all the company in which they work with no employee generated financial outlay. These plans are utilized most often to allow the business founder to sell their business to a buyer (the ESOP trust) so that the founder has a liquidation event and at the same time can maintain the legacy of the operations and transfer out of the company over time. Corporate attorney Louis O. Kelso[3] invented the ESOP concept ~50 years ago so that employees could be part of a growing capital estate which would not only incentivize the employee-owners to work harder to achieve more dividends, but also procure more tax dollars to the IRS. Mr. Kelso’s concept specifically intended for the employees of the ESOP to own the “machines”, and emerging technology, which at the time, were under scrutiny for job elimination. Therefore, if the employee were to no longer be needed in the operations, she/he would still be generating income.

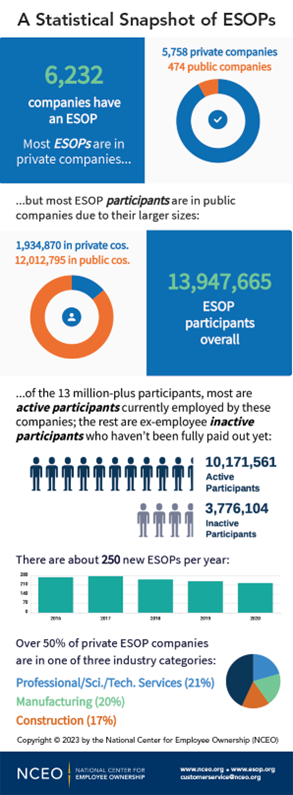

Per the National Center for Employee Ownership (NCEO), there are currently approximately 6,500 ESOPs and nearly 14 million participants (10 million-plus of which are actively working in the company) in the United States.[4] The number and profitability of ESOPs is expected to grow, and creating clear regulations regarding the concept of these plans, i.e., value determination and quantification thereof, will likely encourage even more ESOP growth than is currently forecasted.

DOL Past Attempts at Defining Adequate Consideration

Congress created ERISA section 408(e) of the ERISA and enacted the DOL to issue regulations pertaining to the adequate consideration standard. As a qualified retirement vehicle plan, ERISA section 408(e) notes that the acquisition or sale by a plan of qualifying employer securities does not constitute a prohibited transaction if various requirements are met, including that the sale be for adequate consideration. In 1988, the DOL proposed rulemaking that sought to clarify the meaning of this key terminology via 29 C.F.R. Section 2510-3(18)(b). Section 3(18)(B) defines adequate consideration in the case of an asset, for which there is no generally recognized market, as the fair market value of the asset as determined in good faith by the trustee or named fiduciary pursuant to the terms of the plan and in accordance with the regulations promulgated by the Secretary of Labor of the DOL. In the proposed ruling, fair market value would be defined as the following:

The price at which an asset would change hands between a willing buyer and a willing seller when the former is not under any compulsion to buy and the latter is not under any compulsion to sell, and both parties are able, as well as willing, to trade and are well-informed about the asset and the market for that asset.[5]

The ESOP Association, amongst other ESOP oversight bodies, ESOP trustees, and private and public business owners and employees argue that full potential of ESOP trust owned companies is being stymied since the definition and methodology of key inputs, including fair market value, are murky.[2]

Progress in the Fall of 2023

In April of 2023, the DOL agreed to move forward with data gathering to assist in the legislation of clearly defined ESOP regulations, and in the fall of 2023, a DOL-led public hearing was held. At the meeting, key ESOP stakeholders, the DOL, and others were able to discuss the definition of adequate consideration as part of a legislative act.

Some of the areas of discussion at the public hearing included:

- Definition of fair market value

- Valuation methods impacting fair market value

- Responsibilities of the ESOP trustee

Conclusion

Adequate consideration is the key concept at the nucleus of ESOPs, and obtaining defined regulations as to the way in which this concept is achieved has been an ongoing concern for the many shareholders, associations, and appraisal organizations who work on, and in, ESOPs. On the one hand, the intention behind the proposed regulations seems prudent for ESOP participants, but on the other hand overly stringent legislation may deter the formation and operation of these qualified retirement plans available as an implement for employee ownership. Regardless of the outcome, it is surely going to be an interesting experience for not only those involved in ESOPs, but for the valuation community as a whole, and we will be sure to update the QuickRead and NACVA community accordingly.

[2] https://www.marcumllp.com/insights/esop-association-petitions-congress-on-proposed-regulations-for-adequate-consideration

[1] DOL_Petition_cover_letter_and_petition_FINAL20220922.pdf (assets-tea.s3.us-east-2.amazonaws.com)

[2] Department of Labor Agrees to Notice and Comment Rulemaking on Adequate Consideration Exemption for ESOPs | The ESOP Association

[3] https://www.esopinfo.org/videos/ownership-concepts.php

[4] https://www.esop.org/articles/faqs-esops-employee-ownership.php

[5] chrome-extension://efaidnbmnnnibpcajpcglclefindmkaj/https://www.irs.gov/pub/irs-wd/0930038.pdf

Trisch Garthoeffner, ABV, CVA, MAFF, EA, MAcc, has 20+ years of experience in providing business valuation and financial consulting services. She is an Accredited Business Valuator (ABV) through the AICPA, a Certified Valuation Analyst (CVA) and Master Analyst in Financial Forensics (MAFF) through the NACVA, an IRS representative (Enrolled Agent or EA), and a court certified expert witness. Additionally, she has her master’s in accounting with a concentration in business valuations (MAcc). In 2020, she was nominated as a NACVA Standards Board (SDB) member; in 2021, nominated vice-chair; in 2022, served as chair; and is a current Executive Advisory Board appointed advisor to the SDB. She is a past Florida State Chapter President for NACVA, a current member of the NACVA exam task force (providing teaching for the preparation of the CVA exam for valuation expert candidates nationwide), a board member and quarterly author for the QuickRead periodical, a past treasurer of the Florida Academy of Collaborative Professionals, and a past vice-president of the Southwest Florida Chapter of Collaborative Professionals and current member. In her spare time, she enjoys spending time with her daughter, antiquing, and fostering animals for the local Humane Society.

Ms. Garthoeffner can be contacted at (239) 919-3092 or by e-mail to trisch@anchorbvfs.com.