The 2013 Resurgence of the Dividend Recapitalization

How long will it last?

Dividend recapitalizations provide a mechanism for owners, including private equity firms, to return capital to them (the investors) in lieu of an outright sale. The article discusses trends, the reasons for recapitalizing, and suggests what characteristics to look for when considering this technique.

Dividend Recapitalization

Anticipated changes in the U.S. tax code led to what many thought would be a short-lived spike in dividend recapitalizations in late 2012. Instead, dividend recapitalization activity surged again this year. The appetite of the debt markets has remained strong, leading to favorable pricing and loan terms. Dividend recapitalization transactions totaled $60.2 billion in debt by October 18, 2013, versus $56.4 billion in all of 2012.1

The interplay of several factors has created a “perfect storm” for dividend recapitalizations: private equity (PE) firms returning capital to investors before they embark on fund raising, the relative attractiveness of debt financing compared to other capital-return options, and a low interest rate environment spurring activity in the high-yield debt market.

Return of Capital

PE firms have found dividend recapitalization transactions to be an attractive alternative to outright sale or initial public offerings of shares of portfolio companies. Those avenues have been more difficult to navigate in the current economic cycle, whereas the stability of low interest rates and consequent demand for yield has tipped the balance of probability in favor of a timely execution of a successful recapitalization.

For PE firms, the average holding period of an investment from purchase to exit has increased from 3.9 years in 2008 to 5.0 years in 2012 2 due to economic conditions over the last five years. Over the same period, the average number of years from the time of a leveraged buyout to a dividend recapitalization declined from 3.8 years to 3.2 years.3 Many funds raised during 2006 to 2008 are returning to investors for new commitments. Providing a quick return of capital through a dividend recapitalization increases their chances of successful fundraising while also reserving the option of future economic gains in the company as the economy improves.

Low Interest Rates

As previously mentioned, pricing remains favorable, and many recapitalizations in 2013 have been driven by the continued low interest rate environment. For companies that priced their current facilities during higher interest-rate periods, including certain periods in 2012, there may be an opportunity to re-price at advantageous rates. In September 2013, the weighted average spread for Term Loan B issuances in conjunction with dividend recapitalizations was LIBOR+450 basis points, representing a slight increase from the July average of LIBOR+425 basis points.4 Based on discussion at their most recent meeting, the Federal Reserve’s quantitative easing policy will continue, with the majority of Fed officials predicting that interest rates will remain low into 2015 or 2016.5

High-Yield Debt

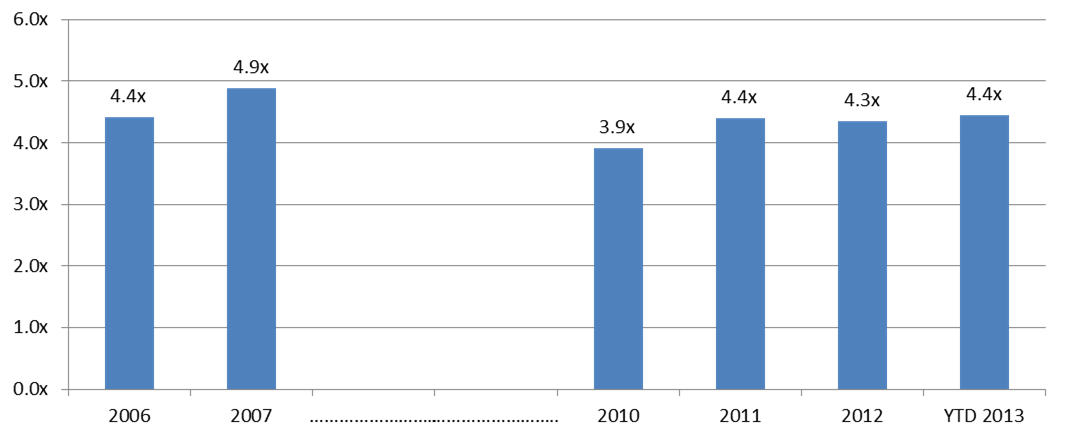

The search for yield has driven many investors to aggressively purchase high-yield debt. The average year-to-date total leverage for dividend recapitalizations was 4.4x EBITDA as of September 30, 2013.6 Companies that completed leverage transactions in prior years at lower leverage multiples or companies that have outperformed EBITDA projections may be able to take on additional leverage and return capital to investors, while keeping debt service payments at the same level. In addition to the amount of credit that is available, we also note that the loan terms are generally less stringent.

Existing debt may warrant a refinancing to obtain more advantageous, covenant-lite terms, such as debt incurrence covenants only (no maintenance covenants), no loan amortization or required cash sweeps.7 These terms may enable the company to weather a downturn by providing an additional cash cushion due to lower debt service requirements. In the third quarter of 2013, nine of the 28 dividend recapitalizations included covenant-lite loans,8 and covenant-lite lending to date has been nearly exclusively to companies with EBITDA greater than $50 million.9

Average Total Debt / EBITDA—Dividend Recapitalizations

Jan. 2006 through Sept. 2013

Can It Continue?

The success of a dividend recapitalization depends on a few key factors. Companies must have demonstrated the ability to weather an economic or operational downturn as well as possess a strong track record of debt service and access to capital markets. The composition and quality of EBITDA is also an important factor. Today, lenders require a deeper understanding of any modifications to reported EBITDA to determine if adjusted EBITDA will generate sustainable cash flow.

As leverage levels have increased in recent years, the Federal Reserve (Fed) has indicated that it is wary of “lax underwriting” for leveraged loans, which prompts the question: are dividend recapitalizations a risky strategy? An article by Moody’s has indicated that while increased leverage may lead to a ratings downgrade based on credit metrics, studies have shown that companies that have undertaken dividend recapitalizations have not had significantly higher default rates than those that have not.10

In addition, sources in the financing industry indicate that more robust diligence is being performed and that lenders are considering the cyclicality of the business to determine the appropriate leverage levels. From a process standpoint, boards continue to rely upon solvency opinions rendered by independent, qualified financial advisors as part of their broader diligence of the transaction prior to approving special distributions funded, in part, by new debt and cash on hand.

Alvarez & Marsal believes that continued demand for investment returns, liquidity in the high-yield debt markets and the low interest rate environment will support dividend recapitalizations. While the pace of activity is expected to slow, we believe that there are opportunities for companies to employ this strategy in the near to medium term.

1 Standard & Poor’s Leveraged Commentary & Data, “Dividend Volume Hits Record Level in 2013, but Slows into Year-End,”, October 18, 2013.

2 Preqin Ltd., “Private Equity-Backed Portfolio Company Holding Periods,” Private Equity Spotlight, May 2013.

3 Standard & Poor’s Leveraged Commentary & Data, “Dividend Volume Hits Record Level in 2013, but Slows into Year-End,” October 18, 2013.

4 S&P Capital IQ LCD US, U.S. Weekly LoanStats Pipeline. “EBITDA is Defined as Earnings before Interest, Taxes, Depreciation, and Amortization Expense

5 “Four Takeaways on the Fed’s Economic and Rate Projections,” The Wall Street Journal, September 18, 2013, http://blogs.wsj.com.

6 S&P Capital IQ LCD, U.S. Weekly LoanStats Pipeline.

7 As defined by S&P CapitalIQ LCD, www.lcdcomps.com.

8 S&P Capital IQ LCD, U.S. Weekly LoanStats Pipeline.

9 Standard & Poor’s Leveraged Commentary & Data, “Middle Market Cov-Lite Update: Utility Services Adds leverage test,” October17, 2013.

10 Moody’s Investors Service, “Announcement: Moody’s: Dividend Recaps Don’t Change the Equation for Investors in the Event of Default,” May 2, 2013.

This article originally appeared in the November 07, 2013 issue of A&M Action Matters.

© Copyright 2013, Alvarez & Marsal Holdings, LLC. Reprinted with permission.

[author] [author_image timthumb=’on’]http://www.alvarezandmarsal.com/sites/default/files/alvarezmarsal-KRussell.jpg[/author_image] [author_info]Kimberly Russell is Managing Director and Lynn Sommer is Senior Director at Alvarez & Marsal’s (A&M) office in New York. [/author_info] [/author]

Related posts

-

HVAC Business Valuation Considerations

-

How Bad Data Hurts Your Valuation

-

Valuations in Private Buy/Sell Transactions

-

2022 M&A in Review

-

The Criticism of the Guideline Private Comparable Transaction Method

-

The Role of Forensic Accountants in Measuring and Detecting Fraud in Employee Loss Claims

-

The Role of Forensic Accountants in Measuring and Detecting Fraud in Employee Loss Claims