The New Revenue Recognition Standard

A Principle-Based Model Revenue Recognition

Wiley author Joanne Flood looks at how the converged revenue standard affects companies reporting under U.S. GAAP.

Accounting Standards Update (ASU) 2014-09—Revenue from Contracts with Customers (Topic 606)—updated 200 separate items of U.S. Financial Accounting Standards Board (FASB) Accounting Standards Codification® (ASC) guidance, most of it industry specific.

Accounting Standards Update (ASU) 2014-09—Revenue from Contracts with Customers (Topic 606)—updated 200 separate items of U.S. Financial Accounting Standards Board (FASB) Accounting Standards Codification® (ASC) guidance, most of it industry specific.

ASU 2014-09 is one of the FASB’s most ambitious projects and was more than ten years in the making. It was issued as a joint project with the International Accounting Standards Board (IASB). Revenue recognition has often been a source of restatements and Securities Exchange Commission (SEC) comments. The FASB believes the final document meets two major goals—simplification of revenue recognition guidance and consistency globally and across markets and industries. The ASU provides a robust framework that is expected to simplify preparation of financial statements by reducing the sources of guidance and replacing it with a single source which users can understand. The ASU also includes new guidance for contract modifications and consistent application for service contracts.

Entities that currently apply entity-specific guidance will see the greatest impact. Industries affected include telecommunication, computer software, construction, aerospace and defense, real estate, licensors (pharmaceuticals, film and entertainment, franchisors), and asset management. Vendor specific objective evidence (VSOE) is no longer required for companies selling software. Entities can use it, but if it is not available, estimates may be used. This is an area that will require a high degree of judgment.

For some but not all of the industries listed above, revenue recognition may be accelerated. For instance, for asset management, revenue may generally be recognized later under the new requirements. In addition, the changes may affect customer loyalty programs. It is expected that entities will be reviewing their loyalty programs to evaluate their effects, if any, on revenue.

The ASU is over 700 pages and was released in three sections:

- Section A—Summary and Amendments That Create Revenue from Contracts with Customers (Topic 606) and Other Assets and Deferred Costs—Contracts with Customers (Subtopic 340-40)

- Section B—Conforming Amendments to Other Topics and Subtopics in the Codification and Status Tables

- Section C—Background Information and Basis for Conclusions

Scope

The following are outside the scope of Topic 606:

- Lease contracts

- Insurance contracts issued by insurance entities within the scope of ASC Topic 944

- Financial instruments and other contractual rights or obligations

- Guarantees other than product or service warranties

- Non-monetary exchanges between entities in the same line of business to facilitate sales to customers or potential customers.

Care should be taken to determine whether a contract is with a customer or if it is a collaborative effort.

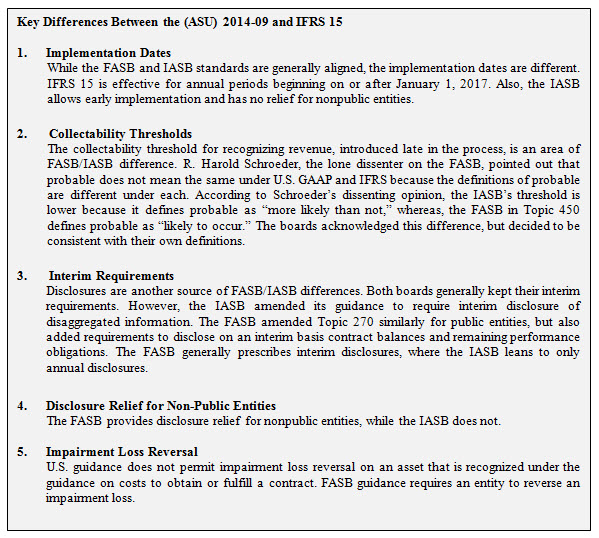

Effective Dates

The FASB decided on a longer-than-usual implementation period because of the number of organizations and line items affected. The ASU is effective in the U.S. as follows:

- For public entities, the guidance in the update is effective for annual reporting periods beginning after December 15 2016, including interim reporting periods within that period. Early application is not permitted.

- For non-public entities, the new guidance will be required for annual reporting periods beginning after December 15, 2017, and interim and annual reporting periods after those reporting periods. A non-public entity may elect early application, but no earlier than the effective date for public entities.

The FASB has on more than one occasion (during the press conference on May 28 and again on a webcast on June 5) appeared to leave the door open to extending the implementation date. However, current consensus is that the FASB has little appetite for extending the dates.

Implementation Options

Entities have the option to implement the guidance through:

- Full retrospective application, or

- Modified retrospective application

The Full Retrospective Approach is transparent and may be effective for entities expecting to recognize revenue earlier. This approach also includes optional practical expedients.

Using the Modified Retrospective Approach, the entity recognizes the cumulative effect of initially adopting the standard as an adjustment to the opening balance of retained earnings in the annual period when the standard is adopted. If the entity issues comparative statements, then it reports revenue for prior years under the guidance in effect before adoption. Additional disclosures are required for entities using this approach.

Note: The standard includes practical expedients in other areas of the guidance for public and nonpublic entities.

Core Principle And Five Steps

The ASU articulates a core principle on which the new guidance is based:

Recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

To achieve this core principle, an entity should follow these five steps:

- Identify the contract with customers. (ASC 606-10-25-1 through 25-13)

- Identify the performance obligations (promises) in the contract. (ASC 606-10-25-14 through 25-22)

- Determine the transaction price. (ASC 606-10-32-2 through 32-27)

- Allocate the transaction price to the performance obligations in the contract. (ASC 606-10-32-28 through 41)

- Recognize revenue when (or as) the reporting organization satisfies a performance obligation. (ASC 606-10-25-23 through 25-30)

In reviewing a transaction, each of the five steps above may not be needed, and they may not always be applied sequentially. Note that the ASU is not organized by these five steps, but the FASB believes the steps offer a methodology for entities to use when deciding the appropriate accounting for a transaction. The model is based on a control approach as opposed to the Risk And Rewards Approach under current U.S. GAAP. However, risk and rewards are a factor when determining control for point in time revenue recognition.

Disclosures

The ASU includes extensive new disclosure requirements designed to provide better information to financial statement users about contracts with customers. The additional disclosures are partially driven by the increased judgment related to estimates required in the new guidance. The requirements are comprehensive and include quantitative and qualitative information to enable users to understand the nature, amount, timing, and uncertainty of revenue and cash flow form contracts with customers. The ASU includes some exceptions for disclosure by nonpublic entities.

SEC

The SEC is currently considering the new guidance. It is expected to adopt the changes and will be keeping a close eye on implementation. The SEC has offered early relief on revenue recognition implementation. Entities electing full retrospective adaption will not be held to a five-year presentation of revenue figures. Shelley Luisi of the SEC’s Office of the Chief Accountant has stated that “they will not object if the retrospective application only applies in selected financial data to the years that are included in the audited financial statements.” Ms. Luisi emphasized that disclosure will be critical to investors understanding the inconsistency.

Other Changes

In addition to the items mentioned above, the ASU includes changes on contract costs, right of returns, warranties, principal vs agent consideration, licenses, repurchase agreements, customer acceptance terms, and other areas.

Transition Resource Group

The FASB and the IASB have established a joint Transition Resource Group (TRG), which aims to inform the boards about potential implementation issues that could arise during the transition period. The boards will then consider whether amendments or additional guidance is needed. The TRG will not issue guidance. The TRG has begun meeting and has discussed issues, such as gross vs. net revenue—intangible goods or services and net amount billed to customers, sales- and usage-based royalties for income statement property for licenses of intellectual property, and impairment testing of capitalized contract costs. The boards will provide a status update on TRG cases on or before October 31, 2014.

Joanne Flood, CPA, is author of Wiley GAAP 2014: Interpretation and Application of Generally Accepted Accounting Principles; Wiley GAAP 2013: Interpretation and Application of Generally Accepted Accounting Principles; Wiley Practitioner’s Guide to GAAS 2013: Covering all SASs, SSAEs, SSARSs, and Interpretations. Ms. Flood specializes in technical guidance and training courses. Her subject matter expertise is in U.S. accounting and auditing standards and International Financial and Reporting Standards. Ms. Flood can be reached at jflood@optonline.net.

Copyright Wiley, 2014. Originally published on Wiley Insight IFRS, the premiere global online community-based subscription service for financial reporting professionals. http://ifrs.wiley.com/.

Related posts

-

Why Strong Internal Controls Are Essential

-

Untangling the Fraud

-

Shannon Pratt’s, The Lawyer’s Business Valuation Handbook 3rd Edition

-

Navigating Capital Structure Assumptions

-

The Meritocracy of an Unregulated Market

-

Intangible Property and Property Tax Appraisals

-

Intangible Property and Property Tax Appraisals

-

Intangible Property and Property Tax Appraisals