Valuation of Ambulatory Surgery Centers

In an Era of Reform (Part I of II)

As demand for healthcare services continues to grow, the site at which these services are performed is experiencing a simultaneous transformation from the inpatient (e.g., hospital) setting to the outpatient setting. This transformation is being driven by factors such as: (1) technological advancements; (2) an increasingly consumer-driven and convenience-driven healthcare delivery environment; (3) pressure from payors; (4) patient demand; and (5) the entrance and diversification of new and different outpatient enterprises. One such example of a growing subset of outpatient enterprises includes ambulatory surgery centers (ASCs). ASCs can be affiliated with a larger hospital or healthcare system, or operated as an independent freestanding facility, and are influenced by certain market forces related to the Four Pillars of Healthcare Valuation, i.e.: (1) regulatory; (2) reimbursement; (3) competition; and (4) technology—each of which relates to almost all aspects of the U.S. healthcare delivery system. This article will review the unique value drivers that impact the typical valuation approaches, methods, and techniques that are often utilized in determining the value of ASCs in the current healthcare delivery system.

Introduction

As demand for healthcare services continues to grow, the site at which these services are performed is experiencing a simultaneous transformation from the inpatient (e.g., hospital) setting to the outpatient setting.[i] This transformation is being driven by factors such as: (1) technological advancements; (2) an increasingly consumer-driven and convenience-driven healthcare delivery environment; (3) pressure from payors; (4) patient demand; and (5) the entrance and diversification of new and different outpatient enterprises. One such example of a growing subset of outpatient enterprises includes ambulatory surgery centers (ASCs). ASCs can be affiliated with a larger hospital or healthcare system, or operated as an independent freestanding facility, and are influenced by certain market forces related to the Four Pillars of Healthcare Valuation, i.e.: (1) regulatory; (2) reimbursement; (3) competition; and (4) technology—each of which relates to almost all aspects of the U.S. healthcare delivery system. This article will review the unique value drivers that impact the typical valuation approaches, methods, and techniques that are often utilized in determining the value of ASCs in the current healthcare delivery system.

Ambulatory Surgery Centers Overview

ASCs are outpatient facilities in which surgeries that do not require inpatient hospital admission, or a length of stay lasting more than 24 hours, may be performed.[ii] ASCs may be classified as single specialty or multi-specialty, and may be owned by hospitals, physicians, or other healthcare enterprises. Note that, according to the Ambulatory Surgery Center Association (ASCA), physicians maintain some amount of ownership in approximately 90% of ASCs.[iii]

Since their inception more than 20 years ago, the number of ASC facilities, as well as the number of procedures performed in ASCs, has expanded significantly, due, in large part, to the advancement of minimally invasive surgical techniques and the shift of the provision of services from the inpatient to the outpatient setting. As of December 2017, there were 5,602 Medicare-licensed ASCs.[iv] Despite significant initial growth, the rate at which new ASCs have been developed has decreased since 2010.[v]

Many patients have reported a favorable opinion of ASCs due to: (1) less paperwork to complete; (2) decreased waiting time; (3) convenient locations; (4) easier scheduling; and (5) lower costs and copayments relative to surgery services provided in an inpatient hospital setting.[vi] Likewise, many physicians have a favorable opinion of ASCs due to: (1) the ability to set and maintain their own schedule; (2) the ability to customize their surgical environment; and (3) the use of specialized staff, which often minimizes turnaround time and maximizes the number of procedures that can be performed.[vii]

Current and Future Trends—Regulatory, Reimbursement, Competition, and Technology

Regulatory

Healthcare organizations face a range of federal and state legal and regulatory constraints, which affect their formation, operation, procedural coding and billing, and transactions. Fraud and abuse laws, specifically those related to the federal Anti-Kickback Statute (AKS) and physician self-referral laws (the Stark Law), may have the greatest impact on the operations of healthcare organizations.

Federal Fraud and Abuse Laws

AKS

Enacted in 1972, the federal AKS makes it a felony for any person to “knowingly and willfully” solicit or receive, or to offer or pay, any “remuneration”, directly or indirectly, in exchange for the referral of a patient for a healthcare service paid for by a federal healthcare program.[viii] Violations of the AKS are punishable by up to five years in prison, criminal fines up to $25,000, or both.[ix] The Medicare and Medicaid Patient & Program Protection Act of 1987 amended the original statute to include exclusion from the Medicare and Medicaid programs as an alternative civil remedy to criminal penalties.[x] Additionally, the Balanced Budget Act of 1997 added a civil monetary penalty of treble damages, or three times the illegal remuneration, plus a fine of $50,000 per violation.[xi] Additionally, interpretation and application of the AKS under case law has created precedent for a regulatory hurdle known as the one purpose test. Under the one purpose test, healthcare providers violate the AKS if even one purpose of the arrangement in question is to offer illegal remuneration.[xii]

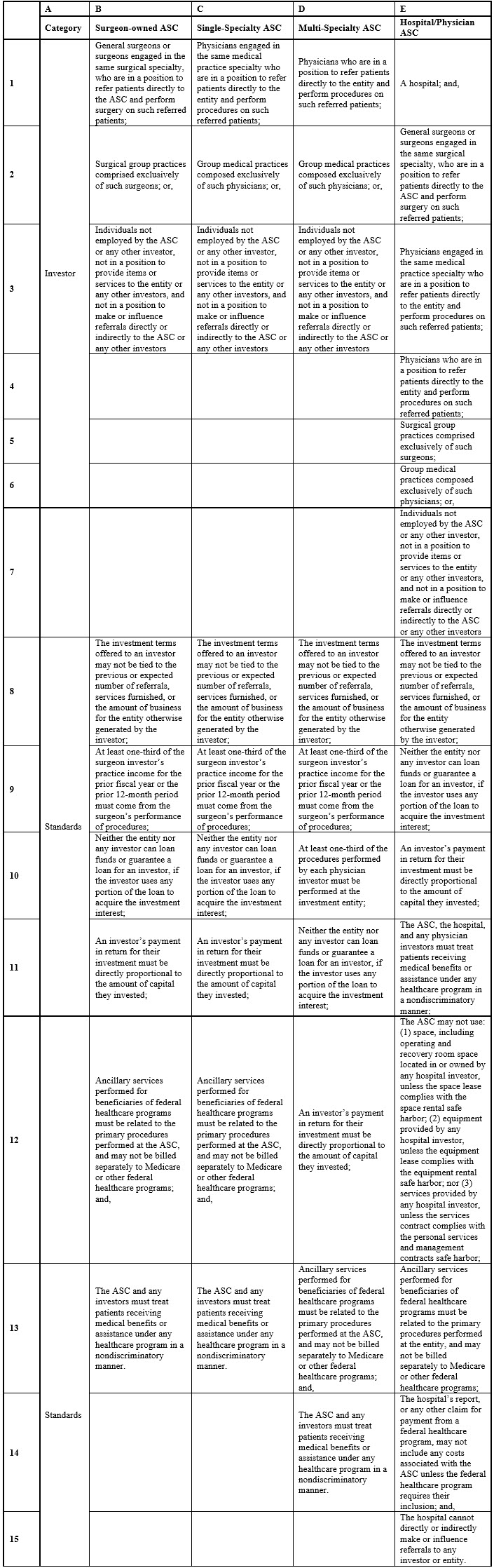

The AKS has a number of safe harbors setting forth regulatory criteria that, if met, shield an arrangement from AKS liability, and are meant to protect transactional arrangements unlikely to result in fraud or abuse.[xiii] ASCs meet the safe harbor provisions under the AKS, provided that payment that is a return on an investment, as long as the entity is legally certified, the operating and recovery room space is exclusively dedicated to the ASC, all patients referred to the entity by an investor are fully informed of the investor’s ownership interest, and all the following applicable standards are met within one of the categories set forth in Table 1, below.[xiv]

Table 1: ASC

Exceptions to the AKS[xv]

Although these exemptions allow federally funded healthcare programs to lessen their liability under the AKS, many business interactions for ASCs may still be suspect under the Stark Law.

Stark Law

The Stark Law prohibits physicians from referring Medicare patients to entities with which the physicians or their family members have a financial relationship for the provision of designated health services (DHS).[xvi]Further, when a prohibited referral occurs, entities may not bill for services resulting from the prohibited referral.[xvii] Under the Stark Law, DHS include: [xviii]

- Certain therapy services, such as physical therapy;

- Radiology and certain other imaging services;

- Radiation therapy services and supplies;

- Outpatient prescription drugs; and

- Inpatient and outpatient hospital services.

Notably, the Stark Law contains many exceptions, which describe ownership interests, compensation arrangements, and forms of remuneration to which the Stark Law does not apply.[xix] Similar to the AKS safe harbors, without these exceptions, the Stark Law may prohibit legitimate business arrangements. It must be noted that in order to meet the requirements of many exceptions related to compensation between physicians and other entities, compensation must: (1) not exceed the range of fair market value; (2) not take into account the volume or value of referrals generated by the compensated physician; and, (3) be commercially reasonable.[xx] Unlike the AKS safe harbors, an arrangement must fall within one of the exceptions in order to be shielded from enforcement of the Stark Law.[xxi]

The regulatory scrutiny of healthcare entities has significantly increased in recent years, and the severe penalties that may be levied against healthcare providers under the AKS or the Stark Law will likely raise a hypothetical investor’s estimate of the risk of investing a new healthcare enterprise, e.g., an ASC, in the current regulatory environment.

Certificate of Need

Certificate of Need (CON) laws are one of the most significant market entrance barriers affecting the U.S. healthcare delivery system. A state CON program is one in which a government determines where, when, and how capital expenditures will be made for public healthcare facilities, services, and major equipment.[xxii] CON requirements are based on the highly contested theory that in an unregulated market, healthcare providers will provide healthcare service using costly technology and equipment, regardless of duplication or need.[xxiii] As of March 2018, 27 states (including Washington, DC) require that ASCs obtain a CON in order to operate within that state.[xxiv]

Reimbursement

ASCs provide technical support services to physicians, such as surgical equipment and supplies, staff, and other services, which enable physicians to perform surgery cases in an outpatient setting. The ASC bills a “facility fee” to the patient or payor for these technical support services, and physicians receive separate professional fee payments for surgical cases, which are billed to the patient or payor.[xxv] Freestanding ASCs often have significantly less overhead than short-term acute care hospitals; therefore, Medicare and third-party payors generally reimburse ASCs at a lower rate relative to hospital payment systems.

For a given service, freestanding ASCs are reimbursed by Medicare at the lower of: (1) the actual charge; or (2) the ASC rate.[xxvi] Freestanding ASCs are reimbursed by Medicare through a percentage of the OPPS for HOPDs, and due to inflation, this is adjusted annually by the conversion factor (CFFor a given service, freestanding ASCs are reimbursed by Medicare at the lower of: (1) the actual charge; or (2) the ASC rate.[xxvii] For a given service, the ASC rate is calculated by multiplying the CF by the ASC relative payment weight, which mimics the relative weight assigned to the service or procedure under the OPPS.[xxviii] Historically, the distinguishing factor between reimbursement payments between HOPDs and freestanding ASCs was the CF because the ASC/HOPD CFs were derived from two different measures of inflation (i.e., hospital market basket for HOPDs and consumer price index for all urban consumers for ASCs), resulting in a widening gap in reimbursement rates between these two entities.[xxix] However, starting 2019, CMS will update the ASC payment rates using the hospital market basket (through at least CY 2023), which it has historically used for updating HOPD payments.[xxx]

Further, Medicare pays ASCs separately for certain ancillary services, including:

- “Drugs and biologicals separately paid under the OPPS;

- Radiology services, integral to the surgical procedure, separately paid under the OPPS;

- Brachytherapy sources;

- Implantable devices with OPPS pass-through status; and

- Corneal tissue acquisition.”[xxxi]

CMS also utilizes an Ambulatory Surgical Center Quality Reporting (ASCQR) Program, which contains eight quality measures and one voluntary measure as of 2018.[xxxii] ASCs that do not meet these requirements receive a payment rate reduced by two percent.[xxxiii]

Competition

Hospital Outpatient Departments (HOPDs)

ASCs typically compete with HOPDs over the technical component revenues from procedures and diagnostic testing provided in these facilities. HOPDs, while typically not “freestanding,” offer many of the same services provided by ASCs and other types of freestanding outpatient enterprises. One reason HOPDs function as significant competitors to ASCs is the financial attractiveness of HOPDs, which receive payment rates 92% higher than ASCs on most surgical procedures.[xxxiv] Significantly, in contrast to ASCs and other freestanding outpatient enterprises, HOPDs typically have access to the market leverage maintained by the parent hospital organization, and are reimbursed under the Hospital OPPS, which allows them to receive a “heightened reimbursement differential” for the same services or procedures provided in an independent freestanding facility. While inpatient discharges declined approximately 21.8% from 2006 to 2016, hospital outpatient visits per beneficiary grew approximately 49% during the same period.[xxxv] It should be noted that many HOPDs are “virtual” outpatient providers, in that they utilize the same physical plant, e.g., certain operating rooms, pre-operative and post-operative, for patients on both an inpatient and an outpatient basis.

However, newer HOPDs do not receive the same reimbursement benefits of previously-constructed HOPDs. The Bipartisan Budget Act of 2015 (BBA) prohibits off-campus HOPDs created after November 2, 2015 from collecting Medicare reimbursement for non-emergency services under the OPPS starting on January 1, 2017.[xxxvi] Effective January 1, 2017, and beyond, these facilities will instead receive reimbursement under an alternative fee schedule, such as the MPFS or the Ambulatory Surgical Center Fee Schedule (ASCFS).[xxxvii]

Physician Practices

ASCs may also face competition from physician practices that perform office-based surgeries and other technical component revenue producing services, e.g., cardiac catheterization services, onsite at the practice. Competition among these providers is likely to further grow as: (1) reimbursement for these services becomes increasingly based on quality versus quantity; and (2) the market for these providers evolves due to increased integration and affiliation among hospitals; physician practices; and other outpatient providers who become affiliated with an accountable care organization (ACO).

General Short-Term Acute Care Hospitals

Some general, short-term acute care hospitals may have competitive advantages over ASCs, including their established managed care contracts; community position; physician loyalty; and geographical convenience for physician inpatient and outpatient practices. However, ASCs compete favorably with general, short-term acute care hospitals on the basis of cost; quality; efficiency; and responsiveness to physician needs in a more comfortable environment for the patient.

ASCs have been able to compete better than community hospitals for more profitable patients by: (1) concentrating only on specific diagnosis-related groups (DRGs); (2) treating far fewer Medicaid patients, who may cost more to treat and generate significantly lower reimbursement yield; and (3) opting out of emergency room departments and services.[xxxviii]

Technology

Continuous advancements in technology, particularly those related to minimally invasive surgery and diagnostic imaging, have allowed procedures which have been traditionally performed in an inpatient setting to be performed in an outpatient setting, such as at an ASC.[xxxix] Minimally invasive surgical procedures typically decrease the risks traditionally associated with surgery through the use of several small incisions to guide fiber-optic cameras to the area(s) of interest.[xl] Laparoscopy, robotic surgery,and other forms of minimally invasive surgeryhave evolved through continuous improvements in surgicaltechnology that have increased ease-of-use, accuracy for the surgeon, andcomfort. For certain high-risk patients (e.g., elderly patients), minimally invasive procedures may be a safer option than traditional surgery because of disproportional operative risks.[xli] However, the price of the required machinery may prevent a small facility from capitalizing on this technology, potentially increasing the difficulty of an independent practice effectively competing with a hospital or a vertically integrated practice.

Conclusion

The value of ASCs is closely tied to the rapidly evolving U.S. healthcare industry, eminent in the modern era of health reform. The ability of ASCs to operate in a continuum of care in the new VBR paradigm may determine their viability as an ongoing enterprise in the future. The number of healthcare services provided at ASCs continues to increase due to rapidly evolving technological advances that allow many services and procedures to be performed in a safe, high quality, and, often, less costly environment than at many inpatient providers. At the same time, the transactional environment of ASCs is also changing as they are increasingly being acquired by hospitals and health systems. Further, in addition to the increased hospital employment of physicians, the overall healthcare transactional market is likely to continue experiencing increased transactional activity as a result of healthcare reform initiatives, as physician practices, and other outpatient enterprises, e.g., ASCs, participate in such integration activities as ACOs, medical homes, and co-management arrangements. Part Two of this two-part series, which will appear in QuickRead, will explore the value drivers of ASCs.

[i] “Hospitals: Origin, Organization, and Performance” in “Health Care USA: Understanding its Organization and Delivery” By Harry A. Sultz and Kristina M. Young, Sixth Edition, Boston, MA: Jones and Bartlett Publishers, 2009, p. 75, 103; “Ambulatory Care” in “Health Care USA: Understanding its Organization and Delivery” By Harry A. Sultz and Kristina M. Young, Sixth Edition, Boston, MA: Jones and Bartlett Publishers, 2009, p. 121–124.

[ii] “Intellimarker: 2018 Multi-Specialty ASC Benchmarking Study” VMG Health: Dallas, TX, 2018, available at: https://intellimarker.com/content/intellimarker/ASC_Overview/ (Accessed 9/18/18), p. 4.

[iii] “Ambulatory Surgery Centers: A Positive Trend in Healthcare” Ambulatory Surgery Center Association, available at: https://www.ascassociation.org/advancingsurgicalcare/aboutascs/industryoverview/apositivetrendinhealthcare (Accessed 9/18/18), p. 1.

[iv] “Intellimarker: 2018 Multi-Specialty ASC Benchmarking Study” VMG Health: Dallas, TX, 2018, available at: https://intellimarker.com/content/intellimarker/ASC_Overview/ (Accessed 9/18/18).

[v] Ibid.

[vi] “Chapter 5

Ambulatory Surgical Centers” In “Medicare Payment Policy: Report to Congress,”

Medicare Payment Advisory Commission, March 2011, (Accessed 06/30/2011), p.

104.

[vii] “2C Ambulatory Surgical Centers” In “Medicare Payment Policy: Report to Congress,” Medicare Payment Advisory Commission, March 2010, http://www.medpac.gov/documents/mar10_entirereport.pdf (Accessed 8/24/11), p. 100.

[viii] “Criminal Penalties for Acts Involving Federal Health Care Programs” 42 U.S.C. § 1320a-7b(b)(1) (2013).

[ix] “Criminal Penalties for Acts Involving Federal Health Care Programs” 42 U.S.C. § 1320a-7b(b)(1) (2013).

[x] “Medicare and Medicaid Patient and Program Protection Act of 1987” Pub. L. No. 100-93, § 2, 101 Stat. 680-681 (August 18, 1987).

[xi] “The Balanced Budget Act of 1997” Pub. L. 105-33, § 4304, 111 Stat. 251, 384 (August 5, 1997).

[xii] “Re: OIG Advisory Opinion No. 15–10” By Gregory E. Demske, Chief Counsel to the Inspector General, Letter to [Name Redacted], July 28, 2015, http://oig.hhs.gov/fraud/docs/advisoryopinions/2015/AdvOpn15-10.pdf (Accessed 12/9/2015), p. 4–5; “U.S. v. Greber” 760 F.2d 68, 72 (3d Cir. 1985).

[xiii] “Medicare and State Health Care Programs: Fraud and Abuse; Clarification of the Initial OIG Safe Harbor Provisions and Establishment of Additional Safe Harbor Provisions Under the Anti-Kickback Statute; Final Rule” Federal Register, Vol. 64, No. 223 (November 19, 1999) p. 63518, 63520.

[xiv] “Exceptions: Ambulatory Surgery Centers” 42 C.F.R. § 1001.952(r) (2015).

[xv] “Exceptions: Ambulatory Surgery Centers” 42 C.F.R. § 1001.952(r) (2015).

[xvi] “CRS Report for Congress: Medicare: Physician Self-Referral (“Stark I and II”)” By Jennifer O’Sullivan, Congressional Research Service, The Library of Congress, July 27, 2004, http://www.policyarchive.org/handle/10207/bitstreams/2137.pdf (Accessed 7/2/2012), p. 1–5; “Limitation on certain physician referrals” 42 U.S.C. §1395nn (2013).

[xvii] “Limitation on certain physician referrals” 42 U.S.C. §1395nn(a)(1)(A) (2013), p. 3058.

[xviii] “Limitation on certain physician referrals” 42 U.S.C. § 1395nn(a)(1)(B) (2013), p. 3064; “Definitions” 42 C.F.R. § 411.351 (October 1, 2014), p. 478–479. Note the distinction in 42 C.F.R. § 411.351 regarding what services are included as DHS: “Except as otherwise noted in this subpart, the term ‘designated health services’ or DHS means only DHS payable, in whole or in part, by Medicare. DHS do not include services that are reimbursed by Medicare as part of a composite rate (for example, SNF Part A payments or ASC services identified at §416.164(a)), except to the extent that services listed in paragraphs (1)(i) through (1)(x) of this definition are themselves payable through a composite rate (for example, all services provided as home health services or inpatient and outpatient hospital services are DHS).”

[xix] “Limitation on certain physician referrals” 42 U.S.C. §1395nn (2013).

[xx] “Fundamentals of the Stark Law and Anti-Kickback Statute” By Asha B. Scielzo, American Health Lawyers Association, Fundamentals of Health Law: Washington, DC, November 2014, https://www.healthlawyers.org/Events/Programs/Materials/Documents/FHL14/scielzo_slides.pdf (Accessed 12/9/2015), p. 28–38.

[xxi] “Health Care Fraud and Abuse: Practical Perspectives” By Linda A. Baumann, Health Law Section of the American Bar Association, Washington, DC: BNA Books, 2002, p. 106.

[xxii] “Improving Health Care: A Dose of Competition: Chapter 8: Miscellaneous Subjects” Federal Trade Commission, Department of Justice, July 2004, https://www.ftc.gov/sites/default/files/documents/reports/improving-health-care-dose-competition-report-federal-trade-commission-and-department-justice/040723healthcarerpt.pdf (Accessed 7/27/16) p. 1.

[xxiii] Ibid, p. 2.

[xxiv] “Intellimarker: 2018 Multi-Specialty ASC Benchmarking Study” VMG Health: Dallas, TX, 2018, available at: https://intellimarker.com/content/intellimarker/ASC_Overview/ (Accessed 9/18/18).

[xxv] “Ambulatory Surgical Center Fee Schedule: Payment System Series” Centers for Medicare and Medicaid Services, December 2017, https://www.cms.gov/Outreach-and-Education/Medicare-Learning-Network-MLN/MLNProducts/downloads/AmbSurgCtrFeepymtfctsht508-09.pdf (Accessed 4/4/18), p. 2–4.

[xxvi] Ibid, p. 5.

[xxvii] Ibid.

[xxviii] Ibid.

[xxix] “Chapter 5: Ambulatory Surgical Center Services” in “Report to Congress: Medicare Payment Policy” Medicare Payment Advisory Commission, March 2018, p. 129.

[xxx] “CMS finalizes Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System changes for 2019 (CMS-1695-FC)” Centers for Medicare & Medicaid Services, November 2, 2018, https://www.cms.gov/newsroom/fact-sheets/cms-finalizes-medicare-hospital-outpatient-prospective-payment-system-and-ambulatory-surgical-center (Accessed 11/2/18).

[xxxi] “Ambulatory Surgical Center Fee Schedule: Payment System Series” Centers for Medicare and Medicaid Services, December 2017, https://www.cms.gov/Outreach-and-Education/Medicare-Learning-Network-MLN/MLNProducts/downloads/AmbSurgCtrFeepymtfctsht508-09.pdf (Accessed 9/18/18), p. 3.

[xxxii] “Chapter 5: Ambulatory Surgical Center Services” in “Report to Congress: Medicare Payment Policy” Medicare Payment Advisory Commission, March 2018, p. 139.

[xxxiii] “CMS finalizes Medicare Hospital Outpatient Prospective Payment System and Ambulatory Surgical Center Payment System changes for 2019 (CMS-1695-FC)” Centers for Medicare & Medicaid Services, November 2, 2018, https://www.cms.gov/newsroom/fact-sheets/cms-finalizes-medicare-hospital-outpatient-prospective-payment-system-and-ambulatory-surgical-center (Accessed 11/2/18).

[xxxiv] “Chapter 5: Ambulatory Surgical Center Services” in “Report to Congress: Medicare Payment Policy” Medicare Payment Advisory Commission, March 2018, p. 136.

[xxxv] “ Chapter 3 Hospital Inpatient and Outpatient Services” In “Report to the Congress: Medicare Payment Policy” Medicare Payment Advisory Commission, March 2018, p. 70.

[xxxvi] “Bipartisan Budget Act of 2015” Public Law 114-74, § 603 (November 2, 2015).

[xxxvii] “Bipartisan Budget Act of 2015” Public Law 114-74 § 603(2)(C) (November 2, 2015); “Section by Section Summary of H.R. 1314” House of Representatives (November 2, 2015) http://docs.house.gov/meetings/RU/RU00/CPRT-114-RU00-D001.pdf (Accessed 4/4/18), p. 6.

[xxxviii] “Could U.S. Hospitals Go the Way of U.S. Airlines?” By Stuart H. Altman, David Shactman, and Efrat Eilat, Health Affairs, Vol. 25, No. 1, (Jan/Feb 2006), p. 19.

[xxxix] “Health, United States, 2006,” National Center for Health Statistics, U.S. Department of Health and Human Services, Hyattsville, (2006), p. 4.

[xl] “Minimally Invasive Surgery” Mayo Clinic, 2018, http://www.mayoclinic.org/minimally-invasive-surgery/ (Accessed 4/4/18).

[xli] “Series of Transcatheter Valve-in-valve Implantations in High-Risk Patients with Degenerated Bioprostheses in Aortic and Mitral Position” By Seiffert, et al., Catheterization and Cardiovascular Intervention, Vol. 76, No. 4, April 19, 2010, p. 608–615; “Elderly Patients in Need of Heart Valve Replacements have Alternative to Surgery” ScienceDaily, June 15, 2010, https://www.sciencedaily.com/releases/2010/06/100615122526.htm (Accessed 4/4/18).

Todd A. Zigrang, MBA, MHA, CVA, ASA, FACHE, is president of Health Capital Consultants, where he focuses on the areas of valuation and financial analysis for hospitals and other healthcare enterprises. Mr. Zigrang has significant physician-integration and financial analysis experience and has participated in the development of a physician-owned, multispecialty management service organizations, and networks involving a wide range of specialties, physician owned hospitals, as well as several limited liability companies for acquiring acute care and specialty hospitals, ASCs, and other ancillary facilities.

Mr. Zigrang can be contacted at (800) 394-8258 or by e-mail to tzigrang@healthcapital.com.

Jessica Bailey-Wheaton, Esq., is Vice President and General Counsel for Heath Capital Consultants where she conducts project management and consulting services related to the impact of both federal and state regulations on healthcare exempt organization transactions, and provides research services necessary to support certified opinions of value related to the Fair Market Value and Commercial Reasonableness of transactions related to healthcare enterprises, assets, and services.

Ms. Bailey-Wheaton can be contacted at (800) 394-8258 or by e-mail to jbailey@healthcapital.com.

Related posts

-

The Perfect Healthcare Storm

-

Federal Judge Strikes Down Ban on Noncompete Agreements

-

SCOTUS Rejects Chevron Deference

-

DOJ Announces Record-Breaking Fraud and Abuse Settlement

-

OPPS Final Rule Issued by CMS

-

CMS Proposes Updates to 2024 Medicare Outpatient Prospective Payment System

-

What Changes to the Lease Accounting Standards Means

-

2021 Healthcare M&A in Review