What discount rate should you use?

Economic damages in litigation must be reduced to present day dollar values to avoid over-compensating the Plaintiff for harm caused by the defendant. This article explains present value theory in simple terms and addresses different methodologies used in reducing future economic damages to a present day dollar value.

I’m often asked to explain present value theory as it relates to the valuation of economic damages in a way that is easily understood. The most effective way to explain this concept is through example:

I’m often asked to explain present value theory as it relates to the valuation of economic damages in a way that is easily understood. The most effective way to explain this concept is through example:

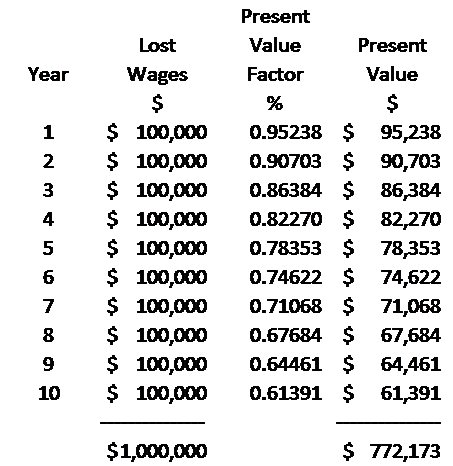

Let us assume we want to value the lost wages of an individual who, absent some cause of action, would have earned a constant $100,000 per year for ten years into the future. The future earnings over this ten-year time period would, therefore, have totaled $1,000,000. If the suit is successful, the plaintiff will receive a lump-sum value of these future payments immediately.

Now, assume that an investment of this lump-sum award could earn 5 percent per year in income. The initial lump sum award plus the income received from investing this award should be enough to replace the $100,000 annual earnings over the next ten years. An analysis of the present value of these ten $100,000 future payments indicates that if the plaintiff invested $772,173 today and earned 5 percent per year, he or she should be able to replace the $100,000 ten-year annual loss with zero dollars left over.

Table 1: Present Value Calculation

Our example assumes a 5 percent rate of return. In order to calculate an appropriate return on investment, one must first decide how the lump-sum award should be invested. The equity market certainly offers higher average returns than does the bond market, but any investment made in the equity market is subject to significant risk. It is for this reason that U.S. Government securities are often used. Courts have also supported the use of discount rates that are considered risk-free in personal injury and wrongful death litigation. Two of the most cited cases supporting the use of risk-free rates are Brown & Root, Inc. v. Desautel, (1977) and Jones & Laughlin Steel Corp. v. Pfeifer, (1983).

The use of risk-free rates is a hotly debated topic in forensic accounting. Earning $100,000 per year for ten years into the future would certainly not have been risk-free. There are certain risks that need to be considered when valuing a future loss of earnings. There is the risk that the plaintiff would have died and not been available to earn this income. There is also the risk that the plaintiff would have voluntarily or involuntarily left the labor force. In addition, there is the risk that the plaintiff would have become unemployed for any number of reasons ranging from downsizing to termination of employment. Economists, litigation support professionals and accountants have found that these risks are better captured in work-life probability offsets rather than in an increased discount rate. Our $772,173 present value figure above would, therefore, be further reduced to account for the risk that our plaintiff would not have realized the $100,000 per year income even absent the cause of action.

The methodology used to discount lost business profits to a present day value differs from that of an individual’s lost earnings. The risk that the business would not have realized a future stream of income is typically captured within the discount rate. The discount rate may include a risk-free rate of return plus a size risk premium, market risk premium, and company specific risk premium. Some analysts use the businesses’ borrowing rate to discount future lost profits while others use the weighted average cost of capital. The valuation of lost profits and lost individual earnings, however, do still require the calculation of a risk-free rate of return.

The appropriate risk-free security to use is widely debated, with no clear guidance from the Courts. Two main considerations, when determining which security to use, are (a) the term of the security and (b) whether to use current rates or some average of historical returns. Some analysts argue for the use of longer-term securities such as ten-year treasury bonds in preference to short-term securities such as three-month treasury bills. In our example above, many economists would argue that ten-year treasury bonds should be used given the ten-year damages period.

Although this argument sounds valid, there are problems with using a longer-term security. Longer term securities have inflation risk, interest rate risk, and, more importantly, liquidity risk. If our plaintiff above invested the $772,173 (we’re ignoring work-life offsets) in ten-year treasury bonds, he or she would not be able to withdraw the funds until maturity ten years later (without penalty, which is not typically accounted for). How will the plaintiff be able to replace the $100,000 income in years one and two (and so forth) if the investment is not liquid? The invested damages award must remain liquid enough to replace the lost earnings when they would have been earned absent the cause of action.

Using current rates instead of an average of historical returns is a method used more often when longer-term securities are chosen. Shorter-term securities require reinvesting. Therefore, when shorter-term securities are chosen, an average of historical rates is typically used. Many analysts argue that the average period used in calculating the discount rate should mirror the damages period. Given our example above, the appropriate discount rate may, therefore, be a ten-year average of the return on short-term treasury bills.

The Board of Governors of the Federal Reserve System provides historical interest rate data online for securities of various types and terms. This data can be found at www.federalreserve.gov/releases/H15/data.htm.

Susan W. Lanham, PhD, MAFF, is owner of Lanham Economics in Scott Depot, West Virginia, and has been working as a forensic accountant for over nineteen years. She has prepared more than 1,000 economic loss valuation reports. She can be contacted at info@lanhameconomics.com.