Unimpeachable Substance and Principles

Business Valuation Standards and the Substance and Principles of USPAP

In this 25th article of the Unimpeachable Neutrality series, the author wants to make a case that he believes is both technically accurate and practically necessary: the business valuation standards of NACVA, ASA, and the AICPA do not merely conform to the substance and principles of USPAP in a passive or derivative sense. They are built upon those principles, share the same foundational architecture, and in the specific context of business valuation, complement USPAP’s framework with discipline-specific structure.

The conversation that the valuation/appraisal profession needs to have is not about which standard is superior. It is about recognizing that the substance and principles behind the standards (the very language embedded in existing law and regulation) already resolve this debate. Every credible business valuation standard meets that threshold. And the most important insight is not that one standard outranks another, but that all of them, properly understood, are built upon the same principled foundation and are speaking the same professional language.

The views expressed in this article are entirely my own, written in my individual capacity as a private practitioner and author. They do not represent, and should not be attributed to, The Appraisal Foundation, the Appraisal Standards Board, the National Association of Certified Valuators and Analysts, the NACVA Standards Board, or any other organization with which I am affiliated. I occupy an unusual position in this profession, and that position is precisely why I have taken exceptional care to write this article as myself, not as a spokesperson for any institution. The boards and organizations I serve are each capable of speaking for themselves, and each has done so through their own formal processes. This article is not their voice. It is mine alone.

I serve as a member of the Appraisal Standards Board of The Appraisal Foundation, the body that promulgates USPAP. I also serve as an advisor to the NACVA Standards Board, the body that promulgates the NACVA Professional Standards and represents the United States on the Global Association of Certified Valuators and Analysts Advisory Council. I am not writing from the perspective of either institution. Further, I am not writing to advance the interests of either institution. I am writing because the profession needs a clear, technically grounded account of how these standards relate to each other.

In this 25th article of the Unimpeachable Neutrality series, I want to make a case that I believe is both technically accurate and practically necessary: the business valuation standards of NACVA, ASA, and the AICPA do not merely conform to the substance and principles of USPAP in a passive or derivative sense. They are built upon the same principles, share the same foundational architecture, and in the specific context of business valuation, complement USPAP’s framework with discipline-specific structure.

Asked and Answered: The Phrase “Substance and Principles”

The phrase “substance and principles” that sits at the center of this debate is not new. The Proposed Amendments to Circular 230, REG-116610-20 employs the “substance and principles” standard expressly, incorporating the functional equivalence framework rather than mandating direct USPAP compliance. Treasury Regulation §1.170A-17 defines “generally accepted appraisal standards” as “the substance and principles of the Uniform Standards of Professional Appraisal Practice.” The proposed amendments to Circular 230 employ the same architecture, requiring that appraisals submitted in administrative proceedings conform to the substance and principles of USPAP.[1] [2] The deliberate selection of this phrasing over “strict compliance” is the central regulatory design choice this article analyzes. That design choice reflects a fundamental regulatory insight: a standard’s value lies in what it requires practitioners to do, not in the language it uses.

What has been lost in the noise surrounding this language is its actual significance. The drafters of these regulations did not require strict compliance with USPAP. They required conformity with its substance and principles. That distinction is not a loophole. It is the considered product of a regulatory framework that recognized, correctly, that multiple credible professional standards can embody the same underlying principles without being identical in form. The “substance and principles” standard is a functional test: does your work product reflect the principles of independence, objectivity, competence, and evidentiary support? It is not a compliance checklist tied to any single standard’s specific language.

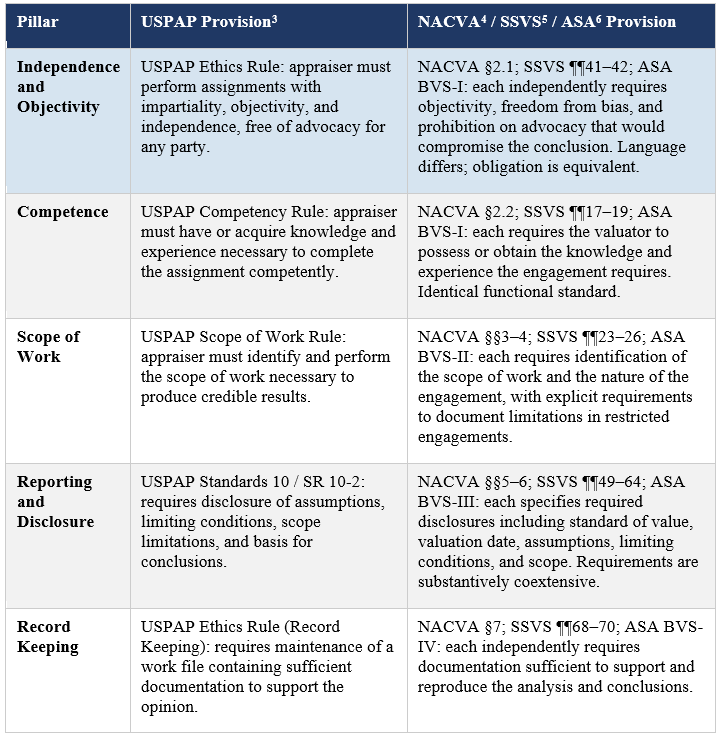

Substantive Pillar Comparison: Specific Provisions, Not Just Categories

The question is not whether NACVA, ASA, or SSVS use the same terminology as USPAP. The question is whether they embody the same principles. And the answer, for each of these frameworks, is unambiguously “yes”. Each requires objectivity. Each requires competence. Each requires that conclusions be credible and supported by appropriate evidence and analysis. Each imposes ethical obligations and disciplinary mechanisms. These are the principles that USPAP embodies. These are the same principles that the credentialing organization standards embody. The “substance and principles” test is satisfied. A comparison of professional frameworks must proceed at the level of specific requirements, not at the level of category labels.

The Proportionality Principle: A Case Against Strict Compliance

The argument against strict compliance is grounded in regulatory principle: proportionality. Where functional equivalence between the “substance and principles” framework and a strict compliance mandate has been demonstrated at the provision level, the less restrictive standard achieves the regulatory goal without the collateral costs of mandatory displacement. Those costs are not theoretical. A strict compliance mandate that displaces NACVA and SSVS would sever the disciplinary relationship between those organizations and the practitioners operating under their standards. The credentialing organizations’ ability to investigate, discipline, and ultimately revoke the credentials of members who violate professional standards depends on those members’ continued engagement with the credentialing framework. Compliance mandates that undermine that engagement do not serve the public. They produce the appearance of more rigorous regulation while dismantling the enforcement mechanisms that protect it.

The proportionality principle in regulatory design is not a novel proposition. It is embedded in federal regulatory review requirements that direct agencies to adopt the approach that achieves the regulatory objective through the least burden consistent with the regulatory objective.[7] [8] [9] Where functional equivalence between the “substance and principles” framework and a strict compliance mandate has been demonstrated at the provision level, the less restrictive standard achieves the regulatory goal without the collateral costs of mandatory displacement. A strict compliance mandate would displace credentialling bodies by severing the disciplinary relationship between those organizations and their practitioners; dismantling the enforcement mechanisms that protect the public, by threat of suspending the very credentials that require professional standards be followed.

Substance and Principle Over Form: Regulatory Primacy

The “substance and principles” framework establishes USPAP in a position of regulatory primacy. USPAP is the reference point against which all other standards are measured. That is an accurate description of the regulatory architecture, and it is the strongest regulatory position a standard can occupy.

It does not follow that the standards are subordinate in every sense. “Subordinate” and “complementary” describe different relational dimensions. The standards are subordinate in the regulatory hierarchy: they derive their legitimacy under §1.170A-17 and Circular 230 from conformity with USPAP’s principles. They are complementary in the professional ecosystem because they provide discipline-specific structure that USPAP’s intentionally broad, multi-discipline design cannot prescribe with the same granularity. Both things are true simultaneously, and the tension between them resolves cleanly once the distinction is clear. The credentialing organizations for business valuation—NACVA, the AICPA, the ASA—developed their standards within that broader framework, translating USPAP’s general principles into discipline-specific requirements. The result is not redundancy or subordination. It is specialization within a principled hierarchy.

My Opinionated Conclusion

Neither public trust nor authority can simply be spoken into existence. They are earned through actions that the profession, the public, and the regulatory system can observe, evaluate, and verify. When our words and actions are centered on accuracy, specificity, and public trust rather than competitive positioning, perception and intention align. That alignment is the unimpeachable position. On balance, the “substance and principles of USPAP” language in current regulation is the correct standard. Any revision substituting “strict compliance” would be technically inaccurate and disproportionate. NACVA Professional Standards, AICPA SSVS, and ASA Business Valuation Standards are built upon the same foundational architecture as USPAP, with substantive equivalence at the provision level in the areas that define USPAP’s core requirements. The question is not about which standard is more rigorous in the abstract. It is about recognizing that discipline-specific standards, by design, add structural features that a broad-discipline framework does not, and cannot, prescribe with the same granularity. It is the natural and appropriate relationship between a principle-based framework and the specialized standards built within it. The question has never been which standard is cited at the top of the report. The question has always been whether the work behind it can withstand scrutiny. That is the test the public cares about. It is also the test that every credible business valuation standard, without exception, is designed to meet.

[1] Treas. Reg. §1.170A-17(a)(2). Generally Accepted Appraisal Standards Defined. Cornell LII (eCFR): https://www.law.cornell.edu/cfr/text/26/1.170A-17. https://www.govinfo.gov/content/pkg/CFR-2020-title26-vol4/pdf/CFR-2020-title26-vol4-sec1-170A-17.pdf

[2] Proposed Amendments to Circular 230, REG-116610-20. Federal Register (Dec. 26, 2024): https://www.federalregister.gov/documents/2024/12/26/2024-29371/regulations-governing-practice-before-the-internal-revenue-service

[3] USPAP Standards 9 and 10, Uniform Standards of Professional Appraisal Practice (2024 ed.). The Appraisal Foundation. Available at: https://www.appraisalfoundation.org/uspap

[4] NACVA Professional Standards (as amended through 2022), §§2–7. Available at: https://www.nacva.com/content.asp?contentid=17

[5] AICPA Statement on Standards for Valuation Services No. 1 (SSVS 1, 2007). Available at: https://www.aicpa-cima.com/resources/download/statement-on-standards-for-valuation-services-ssvs-no-1

[6] ASA Business Valuation Standards (as amended through 2023), BVS-I through BVS-VIII. ASA members performing business valuations are required to comply with both ASA BVS and USPAP concurrently. This concurrent compliance requirement is the strongest available evidence that discipline-specific business valuation standards and USPAP are designed to operate as complementary rather than competing frameworks. Available at: https://www.appraisers.org/Disciplines/Business-Valuation/bv-standards

[7] OMB Circular A-4 (revised 2023) & Executive Order 12866. OMB Circular A-4 (2023 PDF, Biden White House archive): https://bidenwhitehouse.archives.gov/wp-content/uploads/2023/11/CircularA-4.pdf

[8] Federal Register notice of issuance: https://www.federalregister.gov/documents/2023/11/13/2023-24819/issuance-of-revised-omb-circular-no-a-4-regulatory-analysis

[9] Executive Order 12866 (full text PDF, National Archives): https://www.archives.gov/files/federal-register/executive-orders/pdf/12866.pdf

Zachary Meyers, CPA, CVA, is the managing member of C. Zachary Meyers, PLLC, specializing in litigatory accounting and valuation services. He has been retained in over 2,900 matters since 2011, as a testifying expert, consulting expert, or neutral/court appointed expert qualified in forensic accounting, business valuation, pension valuation, and taxation. Mr. Meyers has held multiple influential roles on national and international standard setting bodies, where he has made significant contributions to the financial disciplines at the highest levels of the National Association of Certified Valuators and Analysts (NACVA), Global Association of Certified Valuators and Analysts (GACVA), and The Appraisal Foundation (TAF).

Mr. Meyers can be contacted at (304) 690-2619 or by e-mail to czmcpacva@czmeyers.com.

Related posts

-

Applying the Modern New Business Rule in Real Life

-

Unimpeachable Methodological Consistency

-

AI, Ethics, and Standards in Valuation Practice

-

Engagement Letter Can Make or Break You

-

SBA SOP 50 10 8

-

Clients Turning to AI

-

The Unimpeachable Rebuttal 2.0

-

The Unit Valuation Principle for Property Tax Purposes