Key Takeaways from Professor Aswath Damodaran’s 2026 Edition

Equity Risk Premiums: Determinants, Estimation, and Implications

In March 2026, Professor Aswath Damodaran released the seventeenth edition of his ERP study. Each annual installment incorporates updated market data; changes in macroeconomic conditions; and new research and empirical findings. It is a living dataset and framework that evolves with markets and time. The author provides key takeaways from the 2026 edition.

Overview and Central Thesis

This article provides key takeaways for readers from Professor Aswath Damodaran’s recently released 2026 equity risk premium (ERP) annual update.[1] These annual updates began in 2009.[2] Each installment incorporates updated market data (implied ERP’s, country premiums, etc.); changes in macroeconomic conditions; and new research and empirical findings. It is a living dataset and framework that evolves with markets and time.

To start, below is a brief primer on ERP and foundation of the publication:

The publication centers on the ERP, defined as the additional return investors demand for investing in equities over risk-free assets. Damodaran emphasizes that ERP is not just a theoretical construct but a foundational input in valuation, corporate finance, and investment decision-making. It directly affects discount rates, asset prices, capital allocation, and macroeconomic outcomes.

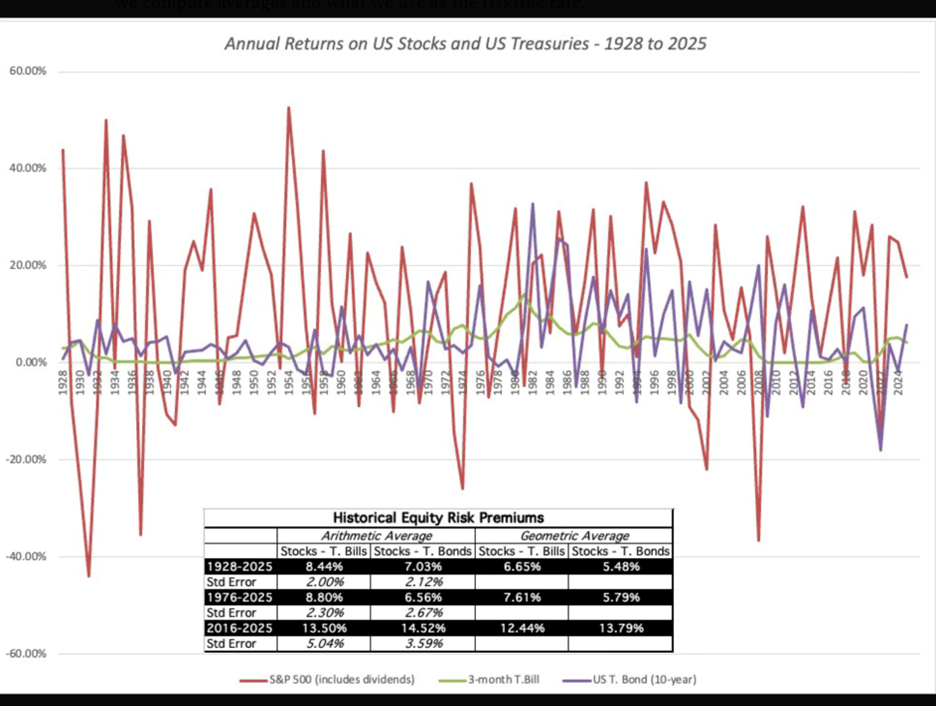

In true “Damodaran-ian” style, the 2026 ERP update focuses upon his data supported opinion with consistent push back on the valuation profession reliance on the use of historical premiums. For those of us who follow Damodaran, this is not a new opinion of his (other published examples noted below).

“… historical equity risk premiums are not only backward-looking and very noisy (see the standard errors), but they allow bias to easily creep in, through the choice of equity risk premiums, with bullish (bearish) analysts picking lower (higher) numbers. Disconcertingly, they also move in the wrong direction, falling during crises (as historical returns get updates) and rising during good times.”[3]

In contrast, Damodaran uses self-published data to estimate ERP using a forward-looking, market-implied approach. Based on his data, the implied U.S. ERP at the beginning of 2026 was approximately 4.23%, reflecting prevailing market conditions, expected cash flows, and the contemporaneous risk-free rate.[4]

In his opinion, this measure reflects the return required by market participants as of the valuation date and is therefore considered more appropriate than historical averages.

Despite its importance, the Paper argues that ERP estimation in practice remains inconsistent and often poorly grounded. If you do not use current implied ERP, you are implicitly making a market timing call, not just a company valuation.

This belief reframes ERP disagreements as:

- Not just technical differences

- But implicit market views

The Paper is structured around three core pillars:

- Why ERP matters and what determines it

- How ERP is estimated in practice

- How practitioners should choose among competing estimates

- Importance of the ERP

At its core, ERP represents the “price of risk” in financial markets. In a hypothetical world of risk-neutral investors, expected returns would equal the risk-free rate. However, because investors are risk-averse, they require compensation for uncertainty, which is embodied in the ERP.

This premium plays a central role in expected return models, including the capital asset pricing model (CAPM) and multifactor models. It influences the cost of equity and cost of capital, making it a critical determinant of firm valuation. A higher ERP increases required returns and lowers asset values, while a lower ERP does the opposite.

Damodaran also highlights ERP’s real-world implications:

- It affects pension funding assumptions and long-term savings decisions

- It influences corporate investment and economic growth

- It plays a role in regulatory pricing (e.g., utilities)

- It underpins asset allocation decisions across stocks, bonds, and real assets

Importantly, debates about whether markets are over- or undervalued can often be reframed as disagreements about the appropriate level of ERP embedded in prices.

- Determinants of the ERP

The Paper identifies ERP as a function of both perceived risk and investor preferences. It is dynamic and influenced by multiple interrelated factors (noted following).

a. Risk Aversion and Investor Characteristics

ERP increases when investors become more risk averse. Factors such as aging populations, lower savings rates, and uncertainty about consumption can raise required premiums. Conversely, more risk-tolerant or forward-looking investors reduce ERP.

b. Macroeconomic Risk

Stable economic environments with predictable growth, inflation, and interest rates tend to have lower ERPs, while volatile or uncertain economies command higher premiums. As noted in the chart above, ERP closely tracks GDP volatility, reinforcing its link to macroeconomic uncertainty.

c. Inflation and Interest Rate Uncertainty

While inflation levels alone may not strongly determine ERP, unexpected inflation and uncertainty about inflation increase risk premiums. Post-2008 dynamics suggest structural shifts, with ERP sometimes moving inversely to interest rates.

d. Information Quality

ERP is affected by the availability, reliability, and interpretation of information. Better transparency reduces uncertainty and lowers ERP, while poor disclosure or ambiguous financial reporting increases it, especially in emerging markets.

e. Liquidity and Market Conditions

Illiquidity raises ERP because investors require compensation for difficulty in exiting positions. Liquidity varies over time and markets, often worsening during crises and amplifying ERP spikes.

f. Catastrophic Risk

Rare but severe events (e.g., financial crises, pandemics) significantly influence ERP. Even if probabilities are low, the potential for large losses leads investors to demand higher premiums. Research cited in the Paper suggests that perceived disaster risk is a major driver of ERP fluctuations.

g. Government Policy and Political Risk

Uncertainty about policy—especially during economic downturns—can elevate ERP. As illustrated by the economic policy uncertainty index,[5] higher policy ambiguity tends to correlate with higher risk premiums.

h. Monetary Policy

Central bank actions, particularly post-2008, may indirectly or directly affect ERP. While lower interest rates theoretically boost asset prices, they can also signal economic risk, potentially increasing ERP.

i. Behavioral Factors

Damodaran acknowledges that ERP is partly shaped by investor psychology, including:

- Inflation illusion (misinterpreting nominal vs. real values)

- Narrow framing (overestimating isolated risks)

- Ambiguity aversion (discomfort with uncertainty)

These behavioral elements contribute to ERP’s variability beyond pure fundamentals.

- The ERP Puzzle

A major academic debate addressed in the Paper is the “ERP puzzle”, the observation that historically high ERPs (e.g., ~6%) cannot be easily explained by standard economic models without assuming unrealistically high-risk aversion.

Proposed explanations include:

- Statistical biases (e.g., survivorship bias in U.S. data)

- Disaster risk models (accounting for rare extreme events)

- Behavioral explanations (e.g., loss aversion)

- Alternative utility frameworks (separating short-term vs. long-term risk preferences)

Damodaran ultimately suggests that the puzzle may reflect limitations of models rather than a true inconsistency in markets.

- Estimation Approaches

The Paper evaluates three primary methods for estimating ERP:

a. Historical Premiums

This approach uses long-term historical differences between stock and bond returns. While widely used, it suffers from:

- Sensitivity to time period selection

- Survivorship bias

- Poor applicability in emerging markets

b. Survey-Based Premiums

Surveys of investors, managers, or academics attempt to capture expected returns. However, these are often:

- Influenced by recent market performance

- Highly variable depending on respondents and framing

- Weak predictors of future returns

c. Implied ERP

This forward-looking approach derives ERP from current market prices using valuation models (e.g., discounted cash flow). Damodaran views this as the most conceptually sound method, as it reflects real-time market expectations.

- Choosing the “Right” ERP

One of the Paper’s key contributions is its discussion of why different methods produce different ERPs and how practitioners should choose among them. Damodaran argues that:

- No single method is universally correct

- The choice depends on context (valuation, geography, data availability)

- Forward-looking (implied) premiums are generally more useful than backward-looking ones

He also dispels common myths, such as the idea that ERP is stable over time or that historical averages are inherently reliable.

Conclusion

Damodaran’s 2026 update reinforces that the ERP is both essential and inherently uncertain. It is shaped by a complex mix of economic fundamentals, market conditions, investor psychology, and methodological choices. For practitioners, the key takeaway is not to seek a single “correct” ERP, but to understand its drivers, limitations, and implications, and to apply it thoughtfully within the context of each analysis.

Ultimately, ERP serves as a unifying concept linking risk, return, and valuation, making it one of the most important, and debated, metrics in finance.

To download the 2026 update, click here.

[1] Referred to throughout herein as the “Paper”.

[2] September 2008 Equity Risk Premium (ERP) (with an October update reflecting the market crisis).

[3] https://aswathdamodaran.substack.com/p/the-price-of-risk-an-equity-risk

[4] https://aswathdamodaran.blogspot.com/2026/01/

[5] Page 21.

Trisch Garthoeffner, ABV, CVA, MAFF, EA, MAcc, has 20+ years of experience in providing business valuation, financial forensic, and merger and acquisition consulting services. In 2020, she was elected to the NACVA Standards Board; in 2021, voted vice-chair; in 2022, voted chair; and is a current Executive Advisory Board advisor for the NACVA Standards Board. She is a past Florida state chapter president for NACVA, a current member of the NACVA exam task force, a board member and quarterly author for the QuickRead valuation periodical, a past treasurer of the Florida Academy of Collaborative Professionals, and a past vice-president of the Southwest Florida Chapter of Collaborative Professionals and current member. In 2024, Ms. Garthoeffner was nominated as a member of Business Valuation Resources (BVR) Leadership Council. On March 06, 2025, she will be in Washington DC with other NACVA representatives[1] to testify regarding NACVA’s collective input regarding the Treasury Department’s proposed rule – Regulations Governing Practice Before the Internal Revenue Service. In her spare time, she enjoys spending time with her daughter, exercising, antiquing, and fostering animals.

Ms. Garthoeffner can be contacted at (239) 919-3092 or by e-mail to trisch@anchorbvfs.com.

[1] T.J. Liles-Tims and Dalton Hopper.

Related posts

-

Are We Taking Our Net Working Capital Calculations Seriously Enough?

-

First Brands

-

Valuation Issues When Quantifying Economic Damages

-

Incorporating Country Risk Premium Differentials

-

Incorporating Country Risk Premium Differentials

-

Best Practices for Estimating the Company-Specific Risk Premium

-

StraightTalk Webinar Series

-

Terminal Values in DCFs